8:00 - 17:00

Opening Hour: Mon - Fri

| Washington Statistics Summary | Details |

|---|---|

| Miles of Roadway | 80,338 |

| Number of Vehicles Registered | 6,489,082 |

| Population | 7,535,591 |

| Most popular vehicle | Outback |

| Uninsured % | 17.4% Rank: 7th |

| Total Driving Related Deaths | Speeding: 172 DUI: 178 |

| Full Coverage Annual Premiums | Liability: $596.67 Collision: $265.74 Comprehensive: $106.38 |

| Cheapest Provider | Allied P&C |

As a Washingtonian, your last, most-difficult decision was probably whether or not to increase the limit on your REI credit card. It’s a challenge to decide which activity to purchase gear for first: hiking Mount Rainier, paddling the Wenatchee, surfing Half Moon Bay, or climbing Frenchman Coulee.

It’s also a challenge to watch auto insurance rates climb as you tirelessly surf the internet to get quotes from as many auto insurance companies as possible so you can get the best deal.

We are here to help you, the Washingtonian weekend warrior, save that energy (and money) for your next outdoor adventure. In this helpful guide, we cover everything about what to know when buying car insurance including coverages, rates, providers, laws, and more.

Saving money on your auto insurance premiums could fund future trips for nature therapy. Start making your comparisons today with just your ZIP code.

Table of Contents

Before we get into examining what affects your rates and the companies to choose from, let’s explore some of the basics.

| Insurance Required | Limits |

|---|---|

| Bodily Injury Coverage | $25,000 per person $50,000 per accident |

| Property Damage Coverage | $10,000 |

Liability auto insurance coverage pays anyone owed compensation when there is an accident you caused.

Washington is a “comparative fault” state, which means if an accident was your fault, you are responsible for all of the damages unless a judge rules that you and the other party share responsibility.

Washington requires that you carry, at the minimum, the following amounts:

Remember, these are the minimum requirements and do not cover injury, death, or damage to yourself or your own passengers.

The state of Washington requires proof of financial responsibility with an insurance company-issued card.

As an alternative to purchasing liability auto insurance, the State of Washington permits its residents to apply for a certificate of deposit through the DOL or a bank.

The certificate must be for a minimum amount of $60,000 to guarantee financial responsibility for an accident. Items of collateral are also an option to fulfill the $60,000 certificate of deposit. You can apply for the certificate at the state’s Department of Licensing.

Another alternative to liability auto insurance and certificate of deposit is a liability or surety bond.

A surety bond is essentially a line of credit in the amount of $60,000 which is the minimum required amount for Washington residents; however, you can obtain a higher amount in a surety bond. Bonds still require premiums, usually at an annual percentage based on your credit score.

The premiums for liability bonds usually range between 1 and 2.5 percent for those with good credit and 10 percent or more for those with bad credit.

Keep in mind, however, that the purpose of a surety bond is to protect you against financial loss in the case that you are at fault and owe reimbursement to the driver who sustained bodily injury and/or property damage.

Most drivers elect to purchase auto insurance because, through the auto insurance company, they can also obtain additional coverage for themselves and their passengers if they are not at fault in an accident.

These coverage types may be personal injury protection, medical payment, comprehensive, and collision, just to name a few.

If you fail to have proof of liability insurance, certificate of deposit, or surety bond, you could face a fine of up to $550 or have your license revoked for three years.

Be sure to always carry proof of insurance, deposit, or bond while you are operating your vehicle.

Are auto insurance rates affordable for residents of Washington?

Short answer: yes, as compared to other states.

In 2014, the annual per capita disposable personal income in Washington was $45,143, which ranks 12th in the nation – not bad.

Disposable personal income (DPI) is the total amount of money available for an individual to spend (or save) after their taxes have been paid.

The average annual cost of auto insurance in Washington is $952 which is just over $30 lower than the national average.

Washington residents pay only 2.11 percent annually of their average DPI. This percent has remained relatively steady while other states such as Michigan increased by just over a half percent in only two years.

The national average is 2.4 percent, so Washington is in a manageable range.

The average Washington resident has $3,762 each month for living expenses. Auto insurance alone will cost about $79 for liability, collision, and comprehensive coverage.

Since our figures above don’t include factors such as your specific annual income, driving record, amount of uninsured coverage, or your chosen deductibles, consider using our calculator to find out what percent your auto insurance is of your monthly income.

CalculatorPro

Why is getting the best deal on auto insurance so important?

American Consumer Credit Counseling suggests saving 20 percent of every paycheck. With Washington’s DPI, that’s about $752 each month! How much are you contributing to your nest egg each month?

The 2015 data from the experts on the matter, the National Association of Insurance Commissioners, tracks average rates for each type of coverage. The most recent data available is in the table below.

| Coverage Types | Annual Costs in 2015 |

|---|---|

| Liability | $596.67 |

| Collision | $265.74 |

| Comprehensive | $106.38 |

| Combined | $968.80 |

From 2011 to 2015, Washington experienced an 8.15 percent increase in average rates which is lower than the nationwide 10 percent rate of increase over the same time period.

Experts recommend drivers purchase more coverage than the minimum because these amounts are not likely to cover the medical bills and repairs or replacement for your vehicle, especially in a comparative fault state like Washington.

But how will additional coverage further protect me and my assets?

This is where profits and losses enter the picture.

Reported profits and losses of auto insurance companies provide an interesting perspective and surface many curiosities about how these companies manage claims for the different types of coverage.

Many of these questions can be answered by looking at loss ratios for each company, which we will examine later. For now, let’s look at state level data.

A loss ratio shows how much a company spends on the types of claims to how much money they take in on premiums. A loss ratio of 60 percent indicates the company spent $60 on claims out of every $100 earned in premiums.

So, the closer the ratio is to 100, the more claims that are paid; however, this also shows that insurance companies are losing money. Sixty to 70 loss ratio is considered to be in the safe zone.

Statewide loss ratios for each coverage type are displayed below.

| Loss Ratio | 2013 | 2014 | 2015 |

|---|---|---|---|

| Personal Injury Protection | 76.62 | 74.19 | 76.77 |

| Medical Payments (Med Pay) | 139.33 | 124.33 | 127.61 |

| Uninsured/Underinsured Motorist | 74.89 | 76.00 | 76.36 |

Personal injury protection (PIP) is an optional add-on for Washington residents. This type of coverage will immediately offset your expenses for time lost at work and your own medical bills (no matter who is at fault) while you wait for your insurance company to process and reimburse for the claim. PIP loss ratios statewide are managed fairly well.

Washington law requires insurance companies to offer personal injury protection to you. If you wish to decline it, you must do so in writing.

However, Med Pay ratios show that Washington auto insurance companies are not managing these claims well. It appears they are losing money paying out claims.

Med Pay is a little different than PIP in that it will provide immediate payment for the medical expenses of passengers in your vehicle after an accident regardless of who is at fault.

In addition, based on the data in the table above, it appears that uninsured and underinsured loss ratios are also in the safe zone. We will take a closer look at these ratios in the next section.

Uninsured motorist coverage has various options in limits of coverage. This type of coverage should come in handy if you are hit by an uninsured driver or if your car is struck by a hit-and-run driver.

At 17.4 percent, Washington ranks 7th out of all 50 states for the highest percentage of uninsured motorists.

You may attribute this high percentage and rank to the option to carry a certificate of deposit rather than purchase a auto insurance policy; however, that couldn’t be further from the truth.

Believe it or not, 32 of the 50 states permit drivers to show proof of financial responsibility via a certificate of deposit; unfortunately, though, very few Americans have between $10,000 (Massachusetts) and $127,000 (Maine) sitting in their savings account to make that kind of investment.

If you have good credit, a liability bond may be an option at lower annual premiums, but that is to cover damages caused to others by you, not damages caused to you by others.

Purchasing a auto insurance policy is more realistic for many Americans with few solid assets, minimal savings, and likely living paycheck to paycheck. Plus, it would take 30 years to pay $60,000 in premiums. Chances are, you will need to file a claim or two within those 30 years, even if you are not at fault.

Again, with over one million uninsured vehicles on Washington’s roads, purchasing an uninsured motorist policy will ensure you have plenty of coverage.

On the other hand, Underinsured motorists coverage will kick in if your medical bills and car repairs or replacement is not completely covered by the at-fault driver who may carry the minimum required amount of liability coverage.

Washington does not currently require uninsured/underinsured motorists coverage, but it is something to closely consider when purchasing your auto insurance policy. Insurance companies in Washington are required to offer this type of coverage to you, but you do have the option to decline it.

We know your goal is to get the complete coverage you need for a reasonable price.

Also, powerful but cheap extras can be added to your policy.

Don’t search for auto insurance without us as your trusty compass! Start comparison shopping today using our FREE online tool. Enter your ZIP code below to get started!

Here’s a list of other useful coverage available to you in Washington:

Age and carrier are the two largest factors that determine rate calculations, as our researchers discovered.

Let’s investigate.

Age, gender, and marital status are some major factors that go into calculating your rate, but there are also other variables in the equation.

In reviewing the top nine carriers that provide auto insurance in Washington, we were able to pull average rates and rank to give you an idea of how these few variables affect the quotes you obtain. Click on the arrows for each column to sort the rates and rank depending upon which range you fall within.

| Company | Single 17-year old female Annual Rate | Single 17-year old male Annual Rate | Single 25-year old female Annual Rate | Single 25-year old male Annual Rate | Married 35-year old female Annual Rate | Married 35-year old male Annual Rate | Married 60-year old female Annual Rate | Married 60-year old male Annual Rate | Average Rate over age 18 Annual Rate | Average Annual Rate under age 18 | Difference in Average Annual Rate |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Allied P&C AXCM | $3,703.82 | $4,511.88 | $1,642.80 | $1,773.07 | $1,379.41 | $1,410.32 | $1,282.59 | $1,334.83 | $1,470.50 | $4,107.85 | $2,637.35 |

| Allstate F&C | $7,306.88 | $8,456.50 | $2,206.95 | $2,292.07 | $2,076.46 | $2,054.07 | $1,919.38 | $2,011.85 | $2,093.46 | $7,881.69 | $5,788.23 |

| American Family Mutual | $7,444.49 | $10,177.95 | $1,958.34 | $2,631.93 | $1,958.34 | $1,958.34 | $1,787.39 | $1,787.39 | $2,013.62 | $8,811.22 | $6,797.60 |

| Farmers Ins Co of WA | $4,781.38 | $5,126.04 | $2,651.77 | $2,761.52 | $2,106.20 | $2,160.58 | $1,928.90 | $2,179.61 | $2,298.10 | $4,953.71 | $2,655.61 |

| First Nat'l Ins Co of America | $9,875.56 | $10,891.02 | $1,909.10 | $2,081.18 | $1,781.98 | $1,950.41 | $1,596.99 | $1,871.63 | $1,865.22 | $10,383.29 | $8,518.08 |

| Geico General | $3,760.90 | $4,926.25 | $2,930.56 | $2,144.04 | $1,741.67 | $1,773.53 | $1,636.13 | $1,636.13 | $1,977.01 | $4,343.58 | $2,366.57 |

| Progressive Direct | $7,688.90 | $8,614.41 | $1,828.39 | $1,821.58 | $1,528.34 | $1,427.27 | $1,374.92 | $1,392.37 | $1,562.15 | $8,151.66 | $6,589.51 |

| State Farm Mutual Auto | $4,512.95 | $5,714.10 | $1,779.29 | $2,045.65 | $1,565.66 | $1,565.66 | $1,407.45 | $1,407.45 | $1,628.53 | $5,113.53 | $3,485.00 |

| USAA | $4,883.26 | $5,777.50 | $1,433.41 | $1,569.85 | $1,133.34 | $1,118.30 | $1,090.31 | $1,091.29 | $1,239.42 | $5,330.38 | $4,090.96 |

| Company | Single 17-year old female Annual Rate | Single 17-year old male Annual Rate | Single 25-year old female Annual Rate | Single 25-year old male Annual Rate | Married 35-year old female Annual Rate | Married 35-year old male Annual Rate | Married 60-year old female Annual Rate | Married 60-year old male Annual Rate |

|---|---|---|---|---|---|---|---|---|

| Allstate F&C | 6 | 6 | 7 | 7 | 8 | 8 | 8 | 8 |

| American Family Mutual | 7 | 8 | 6 | 8 | 7 | 7 | 7 | 6 |

| Farmers Ins Co of WA | 4 | 3 | 8 | 9 | 9 | 9 | 9 | 9 |

| Geico General | 2 | 2 | 9 | 6 | 5 | 5 | 6 | 5 |

| First Nat'l Ins Co of America | 9 | 9 | 5 | 5 | 6 | 6 | 5 | 7 |

| Allied P&C AXCM | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

| Progressive Direct | 8 | 7 | 4 | 3 | 3 | 3 | 3 | 3 |

| State Farm Mutual Auto | 3 | 4 | 3 | 4 | 4 | 4 | 4 | 4 |

| USAA | 5 | 5 | 1 | 1 | 1 | 1 | 1 | 1 |

The three columns to the right in the first table show the average rate for those over 18 compared to those age under 18.

Age is a reasonable influencer in calculating rates; after all, we become more experienced drivers as we get older.

As you can see in the table, if you need to insure a teen driver, Geico or Allied would be good options.

There exists a correlation between rates for teen drivers and risky behavior; the statistics don’t lie when it comes to younger drivers.

The Insurance Institute for Highway Safety (IIHS) released an informative video not too long ago that explains why insurance rates are so high for teens.

The city or even neighborhood in which you live is another factor that influences rates. In most cases, if you live in an urban area, the more likely it is that you will be in an accident.

We include in the tables below the average rate by ZIP code by companies. Feel free to search the table for your current ZIP code and maybe cities to which you plan to relocate.

Let’s start with an overview of the average rates by ZIP code.

| Cheapest ZIP Codes in Washington | City | Average Annual Rate by ZIP Codes | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|---|

| 98368 | PORT TOWNSEND | $2,461.54 | Liberty Mutual | $3,312.18 | American Family | $3,040.02 | Nationwide | $1,820.10 | USAA | $1,912.00 |

| 98382 | SEQUIM | $2,482.65 | Liberty Mutual | $3,343.26 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $1,821.70 |

| 98278 | OAK HARBOR | $2,512.24 | Liberty Mutual | $3,560.47 | American Family | $2,989.30 | USAA | $1,745.19 | Nationwide | $1,891.73 |

| 98362 | PORT ANGELES | $2,515.10 | Liberty Mutual | $3,509.95 | American Family | $3,040.02 | Nationwide | $1,820.10 | USAA | $1,986.87 |

| 98277 | OAK HARBOR | $2,515.42 | Liberty Mutual | $3,560.47 | American Family | $2,989.30 | USAA | $1,726.12 | Nationwide | $1,891.73 |

| 98221 | ANACORTES | $2,528.16 | Liberty Mutual | $3,652.24 | Allstate | $3,111.86 | USAA | $1,711.97 | Nationwide | $1,912.08 |

| 98245 | EASTSOUND | $2,528.40 | Liberty Mutual | $3,442.69 | Allstate | $3,070.79 | Nationwide | $1,870.56 | USAA | $1,890.06 |

| 98261 | LOPEZ ISLAND | $2,534.30 | Liberty Mutual | $3,423.17 | Allstate | $3,111.86 | Nationwide | $1,870.56 | USAA | $1,890.06 |

| 98326 | CLALLAM BAY | $2,535.13 | Liberty Mutual | $3,472.71 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| 98363 | PORT ANGELES | $2,536.42 | Liberty Mutual | $3,598.12 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| 98339 | PORT HADLOCK | $2,540.36 | Liberty Mutual | $3,469.33 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,068.16 |

| 98250 | FRIDAY HARBOR | $2,541.29 | Liberty Mutual | $3,624.73 | Allstate | $3,111.86 | USAA | $1,765.85 | Nationwide | $1,870.56 |

| 98325 | CHIMACUM | $2,546.91 | Liberty Mutual | $3,464.63 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,051.90 |

| 98239 | COUPEVILLE | $2,547.28 | Liberty Mutual | $3,567.99 | Progressive | $3,000.27 | Nationwide | $1,891.73 | USAA | $1,962.49 |

| 98331 | FORKS | $2,548.79 | Liberty Mutual | $3,630.14 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| 98305 | BEAVER | $2,560.25 | Liberty Mutual | $3,718.88 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| 98225 | BELLINGHAM | $2,560.50 | Liberty Mutual | $3,468.06 | American Family | $3,215.37 | USAA | $1,897.96 | Nationwide | $1,937.63 |

| 98226 | BELLINGHAM | $2,564.69 | Liberty Mutual | $3,376.85 | American Family | $3,226.63 | Nationwide | $1,937.63 | USAA | $1,998.33 |

| 99163 | PULLMAN | $2,567.07 | Liberty Mutual | $3,688.52 | American Family | $3,494.22 | USAA | $1,760.55 | Nationwide | $1,794.51 |

| 99136 | HAY | $2,568.28 | Liberty Mutual | $3,688.52 | American Family | $3,310.40 | Nationwide | $1,794.51 | State Farm | $1,952.71 |

| 99333 | HOOPER | $2,570.68 | Liberty Mutual | $3,688.52 | Allstate | $3,485.59 | USAA | $1,760.55 | Nationwide | $1,794.51 |

| 98857 | WARDEN | $2,571.68 | Liberty Mutual | $3,483.46 | American Family | $3,310.40 | Nationwide | $1,822.61 | USAA | $1,921.87 |

| 99111 | COLFAX | $2,575.68 | Liberty Mutual | $3,688.52 | American Family | $3,434.49 | Nationwide | $1,794.51 | State Farm | $1,952.71 |

| 98365 | PORT LUDLOW | $2,577.28 | Liberty Mutual | $3,611.58 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,051.90 |

| 99125 | ENDICOTT | $2,580.52 | Liberty Mutual | $3,688.52 | American Family | $3,434.49 | Nationwide | $1,794.51 | State Farm | $1,952.71 |

Port Townsend has the cheapest ZIP code. Next, the most expensive ZIP codes.

| Most Expensive ZIP Codes in Washington | City | Average Annual Rate by ZIP Code | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|---|

| 98118 | SEATTLE | $4,079.23 | American Family | $5,926.17 | Liberty Mutual | $5,257.26 | USAA | $2,872.67 | Nationwide | $2,911.83 |

| 98108 | SEATTLE | $4,032.13 | American Family | $5,698.95 | Liberty Mutual | $5,084.70 | USAA | $2,820.35 | Nationwide | $2,911.83 |

| 98168 | SEATTLE | $3,956.75 | American Family | $5,534.73 | Liberty Mutual | $5,133.20 | USAA | $2,534.97 | Nationwide | $2,796.55 |

| 98144 | SEATTLE | $3,947.84 | American Family | $5,269.57 | Liberty Mutual | $4,923.17 | USAA | $2,730.82 | Nationwide | $2,911.83 |

| 98106 | SEATTLE | $3,946.95 | American Family | $5,269.57 | Liberty Mutual | $5,121.42 | USAA | $2,781.61 | Nationwide | $2,911.83 |

| 98126 | SEATTLE | $3,946.53 | Liberty Mutual | $5,427.31 | American Family | $5,269.57 | USAA | $2,689.39 | Nationwide | $2,911.83 |

| 98178 | SEATTLE | $3,918.31 | American Family | $5,260.03 | Liberty Mutual | $5,020.17 | Nationwide | $2,796.55 | USAA | $2,915.44 |

| 98404 | TACOMA | $3,907.01 | Liberty Mutual | $5,237.40 | Allstate | $4,925.98 | Nationwide | $2,620.93 | USAA | $2,877.60 |

| 98158 | SEATTLE | $3,898.72 | American Family | $5,534.73 | Liberty Mutual | $5,156.82 | USAA | $2,471.62 | Nationwide | $2,694.23 |

| 98444 | TACOMA | $3,875.05 | Liberty Mutual | $5,480.53 | Allstate | $4,797.69 | Nationwide | $2,620.93 | USAA | $2,744.14 |

| 98188 | SEATTLE | $3,869.30 | American Family | $5,534.73 | Liberty Mutual | $5,300.63 | USAA | $2,471.62 | Nationwide | $2,703.77 |

| 98447 | TACOMA | $3,857.85 | Liberty Mutual | $5,480.53 | Allstate | $4,797.69 | Nationwide | $2,620.93 | USAA | $2,744.14 |

| 98408 | TACOMA | $3,852.24 | Liberty Mutual | $5,287.27 | Allstate | $4,925.98 | Nationwide | $2,620.93 | USAA | $2,796.05 |

| 98134 | SEATTLE | $3,831.61 | American Family | $5,269.57 | Liberty Mutual | $5,247.71 | Nationwide | $2,575.17 | GEICO | $2,580.97 |

| 98136 | SEATTLE | $3,812.97 | American Family | $5,260.03 | Liberty Mutual | $4,990.17 | USAA | $2,654.45 | State Farm | $2,911.32 |

| 98146 | SEATTLE | $3,812.22 | American Family | $5,260.03 | Liberty Mutual | $4,800.78 | USAA | $2,694.59 | Nationwide | $2,796.55 |

| 98057 | RENTON | $3,790.67 | American Family | $5,260.03 | Liberty Mutual | $5,163.65 | Nationwide | $2,571.50 | USAA | $2,813.89 |

| 98409 | TACOMA | $3,787.39 | Liberty Mutual | $5,101.97 | Allstate | $4,598.34 | Nationwide | $2,620.93 | USAA | $2,808.78 |

| 98055 | RENTON | $3,776.55 | American Family | $5,260.03 | Liberty Mutual | $5,163.65 | Nationwide | $2,571.50 | USAA | $2,813.89 |

| 98422 | TACOMA | $3,774.49 | Allstate | $4,925.98 | Liberty Mutual | $4,907.14 | Nationwide | $2,620.93 | USAA | $2,705.65 |

| 98023 | FEDERAL WAY | $3,772.89 | Liberty Mutual | $4,827.97 | American Family | $4,646.13 | Nationwide | $2,786.48 | USAA | $2,792.23 |

| 98418 | TACOMA | $3,770.43 | Liberty Mutual | $5,287.27 | Allstate | $4,598.34 | USAA | $2,296.38 | Nationwide | $2,620.93 |

| 98031 | KENT | $3,768.74 | Liberty Mutual | $4,856.97 | American Family | $4,818.72 | Nationwide | $2,703.77 | USAA | $2,708.12 |

| 98166 | SEATTLE | $3,768.14 | American Family | $5,132.10 | Liberty Mutual | $4,964.65 | USAA | $2,549.27 | Nationwide | $2,694.23 |

| 98125 | SEATTLE | $3,765.22 | American Family | $5,088.26 | Liberty Mutual | $5,068.33 | USAA | $2,673.53 | Nationwide | $2,705.40 |

The more urban areas like Seattle and Spokane will tend to have higher rates than cities in rural areas, even if it is only by a few dollars per month.

For this reason, we include below the average rates by city.

| Cheapest Cities in Washington | Average Annual Rate by City | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|

| Port Townsend | $2,461.54 | Liberty Mutual | $3,312.18 | American Family | $3,040.02 | Nationwide | $1,820.10 | USAA | $1,912.00 |

| Carlsborg | $2,482.64 | Liberty Mutual | $3,343.26 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $1,821.70 |

| Whidbey Island Station | $2,512.24 | Liberty Mutual | $3,560.47 | American Family | $2,989.30 | USAA | $1,745.19 | Nationwide | $1,891.73 |

| Oak Harbor | $2,515.42 | Liberty Mutual | $3,560.47 | American Family | $2,989.30 | USAA | $1,726.12 | Nationwide | $1,891.73 |

| Port Angeles | $2,525.76 | Liberty Mutual | $3,554.04 | American Family | $3,040.02 | Nationwide | $1,844.45 | USAA | $1,970.58 |

| Anacortes | $2,528.16 | Liberty Mutual | $3,652.24 | Allstate | $3,111.86 | USAA | $1,711.97 | Nationwide | $1,912.08 |

| Eastsound | $2,528.40 | Liberty Mutual | $3,442.69 | Allstate | $3,070.79 | Nationwide | $1,870.56 | USAA | $1,890.06 |

| Lopez Island | $2,534.30 | Liberty Mutual | $3,423.17 | Allstate | $3,111.86 | Nationwide | $1,870.56 | USAA | $1,890.06 |

| Clallam Bay | $2,535.12 | Liberty Mutual | $3,472.71 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| Port Hadlock-Irondale | $2,540.36 | Liberty Mutual | $3,469.33 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,068.16 |

| Friday Harbor | $2,541.29 | Liberty Mutual | $3,624.73 | Allstate | $3,111.86 | USAA | $1,765.85 | Nationwide | $1,870.56 |

| Chimacum | $2,546.91 | Liberty Mutual | $3,464.63 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,051.90 |

| Coupeville | $2,547.28 | Liberty Mutual | $3,567.99 | Progressive | $3,000.27 | Nationwide | $1,891.73 | USAA | $1,962.49 |

| Forks | $2,548.79 | Liberty Mutual | $3,630.14 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| Beaver | $2,560.25 | Liberty Mutual | $3,718.88 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| Hay | $2,568.28 | Liberty Mutual | $3,688.52 | American Family | $3,310.40 | Nationwide | $1,794.51 | State Farm | $1,952.71 |

| Bellingham | $2,569.25 | Liberty Mutual | $3,407.26 | American Family | $3,219.12 | Nationwide | $1,937.63 | USAA | $1,971.40 |

| Hooper | $2,570.67 | Liberty Mutual | $3,688.52 | Allstate | $3,485.59 | USAA | $1,760.55 | Nationwide | $1,794.51 |

| Warden | $2,571.68 | Liberty Mutual | $3,483.46 | American Family | $3,310.40 | Nationwide | $1,822.61 | USAA | $1,921.87 |

| Colfax | $2,575.68 | Liberty Mutual | $3,688.52 | American Family | $3,434.49 | Nationwide | $1,794.51 | State Farm | $1,952.71 |

| Port Ludlow | $2,577.28 | Liberty Mutual | $3,611.58 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,051.90 |

| Endicott | $2,580.52 | Liberty Mutual | $3,688.52 | American Family | $3,434.49 | Nationwide | $1,794.51 | State Farm | $1,952.71 |

| Marrowstone | $2,580.67 | Liberty Mutual | $3,520.43 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,068.16 |

| Sekiu | $2,586.92 | Liberty Mutual | $3,868.27 | American Family | $3,040.02 | Nationwide | $1,868.80 | USAA | $1,954.28 |

| Quilcene | $2,587.08 | Liberty Mutual | $3,885.74 | American Family | $3,076.05 | Nationwide | $1,820.10 | USAA | $2,051.90 |

The next table shows the most expensive cities for auto insurance.

| Most Expensive Cities in Washington | Average Annual Rate by City | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|

| Boulevard Park | $3,994.44 | American Family | $5,616.84 | Liberty Mutual | $5,108.95 | USAA | $2,677.66 | Nationwide | $2,854.19 |

| Bryn Mawr-Skyway | $3,918.31 | American Family | $5,260.03 | Liberty Mutual | $5,020.17 | Nationwide | $2,796.55 | USAA | $2,915.44 |

| Midland | $3,907.01 | Liberty Mutual | $5,237.40 | Allstate | $4,925.98 | Nationwide | $2,620.93 | USAA | $2,877.60 |

| Parkland | $3,875.04 | Liberty Mutual | $5,480.53 | Allstate | $4,797.69 | Nationwide | $2,620.93 | USAA | $2,744.14 |

| SEATAC | $3,869.30 | American Family | $5,534.73 | Liberty Mutual | $5,300.63 | USAA | $2,471.62 | Nationwide | $2,703.77 |

| Renton | $3,783.61 | American Family | $5,260.03 | Liberty Mutual | $5,163.65 | Nationwide | $2,571.50 | USAA | $2,813.89 |

| Browns Point | $3,774.49 | Allstate | $4,925.98 | Liberty Mutual | $4,907.14 | Nationwide | $2,620.93 | USAA | $2,705.65 |

| Burien | $3,771.66 | American Family | $5,217.39 | Liberty Mutual | $4,889.82 | USAA | $2,571.83 | Nationwide | $2,728.33 |

| Algona | $3,750.43 | Liberty Mutual | $5,177.43 | American Family | $4,593.45 | Nationwide | $2,633.52 | USAA | $2,747.15 |

| Federal Way | $3,749.88 | Liberty Mutual | $4,761.79 | American Family | $4,603.10 | Nationwide | $2,786.48 | USAA | $2,860.16 |

| Kent | $3,726.02 | Liberty Mutual | $4,762.20 | American Family | $4,760.96 | Nationwide | $2,668.65 | USAA | $2,790.43 |

| Seattle | $3,724.65 | American Family | $5,076.81 | Liberty Mutual | $5,060.37 | USAA | $2,613.06 | Nationwide | $2,687.32 |

| East Hill-Meridian | $3,721.61 | Liberty Mutual | $4,836.29 | American Family | $4,750.66 | Nationwide | $2,637.64 | USAA | $2,674.33 |

| Auburn | $3,710.10 | Liberty Mutual | $4,833.42 | American Family | $4,658.57 | Nationwide | $2,633.52 | USAA | $2,773.88 |

| Tacoma | $3,707.36 | Liberty Mutual | $4,982.08 | Allstate | $4,662.26 | Nationwide | $2,620.93 | USAA | $2,647.08 |

| Newcastle | $3,706.71 | Liberty Mutual | $4,895.49 | American Family | $4,682.60 | Nationwide | $2,579.34 | USAA | $2,604.43 |

| Seahurst | $3,698.19 | Liberty Mutual | $4,964.65 | Allstate | $4,399.28 | USAA | $2,635.41 | Nationwide | $2,694.23 |

| Covington | $3,694.80 | Liberty Mutual | $5,028.45 | American Family | $4,673.55 | Nationwide | $2,625.11 | USAA | $2,706.99 |

| Des Moines | $3,694.01 | American Family | $5,132.10 | Liberty Mutual | $4,586.21 | USAA | $2,551.88 | Nationwide | $2,703.77 |

| Clover Creek | $3,677.71 | Liberty Mutual | $5,138.08 | Allstate | $4,676.26 | Nationwide | $2,620.93 | USAA | $2,713.67 |

| Milton | $3,654.19 | Allstate | $5,160.65 | Liberty Mutual | $4,584.59 | Nationwide | $2,601.58 | USAA | $2,756.13 |

| Pacific | $3,650.77 | American Family | $4,721.34 | Liberty Mutual | $4,482.65 | Nationwide | $2,633.52 | USAA | $2,747.15 |

| Waller | $3,643.68 | Allstate | $5,002.33 | Liberty Mutual | $4,985.35 | Nationwide | $2,620.93 | USAA | $2,743.96 |

| Fife | $3,639.40 | Allstate | $4,925.98 | Liberty Mutual | $4,741.12 | Nationwide | $2,601.58 | USAA | $2,732.13 |

| Lakewood | $3,626.43 | Allstate | $4,730.41 | Liberty Mutual | $4,636.39 | USAA | $2,577.37 | Nationwide | $2,620.93 |

Our data analysts pulled data for the 10 largest insurance companies in Washington to help you begin to make some comparisons and choose the right company and coverage for you and your family when the unexpected happens.

Let’s get started.

| Property & Casualty Insurance | Number |

|---|---|

| Domestic | 7 |

| Foreign | 864 |

| Total | 871 |

The table and chart below shows the ten largest Washington auto insurance companies. The table includes market share, direct premiums written, and loss ratio for 2017. The table is sorted by market share; however, you can sort as you like.

| Company | Direct Premiums Written | Loss Ratio | Market Share |

|---|---|---|---|

| State Farm Group | $867,121 | 66.82% | 16.75% |

| Geico | $563,543 | 73.35% | 10.89% |

| Liberty Mutual Group | $549,853 | 66.42% | 10.62% |

| Allstate Insurance Group | $485,508 | 55.27% | 9.38% |

| Progressive Group | $440,839 | 62.83% | 8.52% |

| USAA Group | $406,048 | 79.28% | 7.85% |

| Farmers Insurance Group | $384,645 | 59.54% | 7.43% |

| PEMCO Mutual Insurance Co | $287,313 | 66.30% | 5.55% |

| American Family Insurance Group | $178,684 | 78.07% | 3.45% |

| Hartford Fire & Casualty Group | $127,979 | 73.22% | 2.47% |

Keep in mind that these loss ratios are for all coverage types combined. It appears that all 10 companies are doing fairly well in managing their loss ratios.

Reviewing ratings provided by third-party entities such as A.M. Best is a third party entity that provides ratings for companies. This is a great place to start in considering which company is right for you. These agencies take into consideration many factors that lead to their judgment of a company’s credibility and financial outlook.

| Company | Financial Rating |

|---|---|

| Allstate Insurance Group | A+ |

| American Family Insurance Group | A |

| Farmers Insurance Group | A |

| Geico | A++ |

| Hartford Fire & Casualty Group | A+ |

| Liberty Mutual Group | A |

| PEMCO Mutual Insurance Co | B++ |

| Progressive Group | A+ |

| State Farm Group | A++ |

| USAA Group | A++ |

Customer satisfaction is just as valuable as a company’s future financial stability.

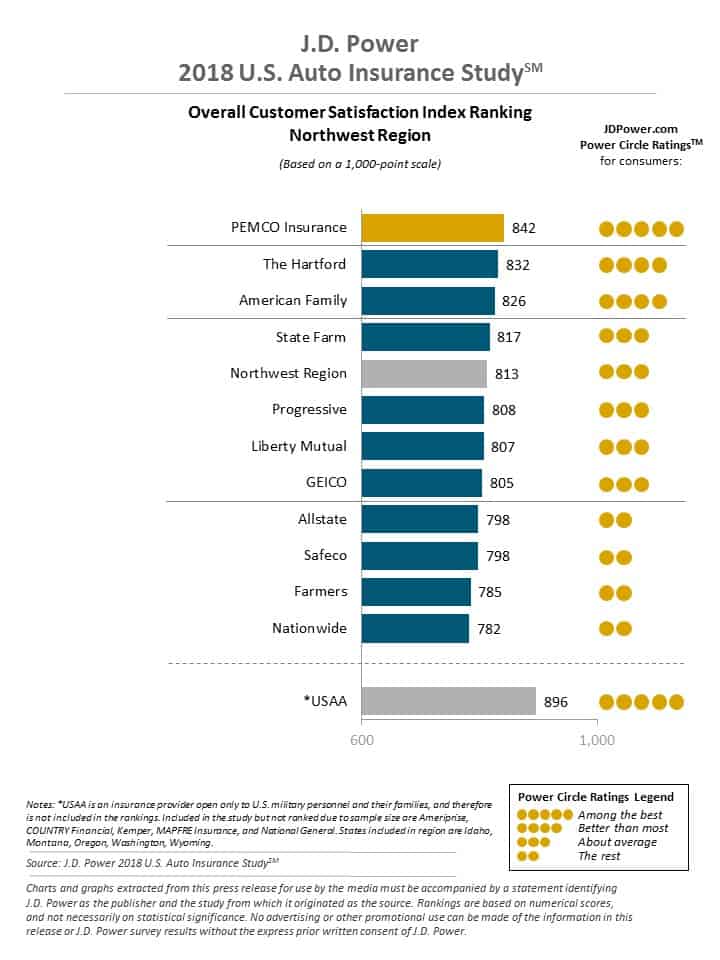

JD Power Power Circle Ratings administers surveys to consumers of a company’s products and services. They look at a wide variety of customer satisfaction variables. The ratings below cover the northwest region which is comprised of five states to include Washington.

Weighing the good and bad about companies is needed to make the best judgment.

The table below shows each company’s total written premium, market share, and complaint index.

A company with a complaint index of one has an average number of complaints. A company with a complaint index higher than one has more complaints than average. The table is sorted based on the lowest complaint ratio. Feel free to sort the table.

| Company | Total Written Premiums | Market Share | Complaint Index |

|---|---|---|---|

| PEMCO | $241,117,743.00 | 6.21% | 0.32 |

| USAA | $305,062,128.00 | 7.84% | 0.7 |

| Liberty Mutual | $230,145,789.00 | 5.92% | 0.75 |

| Allstate | $366,012,635.00 | 9.41% | 0.86 |

| Progressive | $342,488,473.00 | 8.81% | 0.93 |

| State Farm | $609,783,669.00 | 15.70% | 0.95 |

| Geico | $317,701,791.00 | 8.17% | 1.41 |

| American Family | $141,720,830.00 | 3.64% | 1.66 |

| Hartford | $124,577,952.00 | 3.18% | 2.14 |

| Farmers | $328,423,998.00 | 8.45% | 31.65 |

As you can see, just because a company is leading the market in Washington doesn’t mean all of its customers are satisfied.

If you would like to file an official complaint, you can do so with the Office of the Insurance Commissioner.

Now to the rates you’ve been waiting for.

Have you ever wondered how insurance companies determine your precise rate? Other than age, gender, and marital status, your commute, driving record, credit history, and chosen coverage levels also affect your rates.

Before we get to the factors listed above, let’s look at the average rates by the company overall.

| Company | Average Annual Rate | Higher/Lower Rate than State Average | Higher/Lower Percentage than State Average |

|---|---|---|---|

| Allstate | $3,540.52 | $553.83 | 15.64% |

| American Family | $3,713.02 | $726.33 | 19.56% |

| Farmers | $2,962.00 | -$24.69 | -0.83% |

| Geico | $2,568.65 | -$418.04 | -16.27% |

| First National | $3,994.73 | $1,008.04 | 25.23% |

| Allied P&C | $2,129.84 | -$856.85 | -40.23% |

| Progressive | $3,209.52 | $222.83 | 6.94% |

| State Farm | $2,499.78 | -$486.91 | -19.48% |

| USAA | $2,262.16 | -$724.53 | -32.03% |

The state average rate is $2,986.69. The table shows a calculation in dollars and percent of how much higher or lower a company’s rate is than the state average of $2,986.69.

As you can see, USAA and Allied have the best rates compared to the state average. Note that USAA offers services to only active and retired military and their family members. If this doesn’t apply to you, Allied may be a good option.

| Company | 10 miles commute 6,000 annual mileage | 25 miles commute 12,000 annual mileage |

|---|---|---|

| Allstate | $3,540.52 | $3,540.52 |

| American Family | $3,636.77 | $3,789.27 |

| Farmers | $2,962.00 | $2,962.00 |

| Geico | $2,536.39 | $2,600.92 |

| Liberty Mutual | $3,994.73 | $3,994.73 |

| Progressive | $3,209.52 | $3,209.52 |

| State Farm | $2,431.07 | $2,568.48 |

If you have a long commute, getting a policy with Allstate, Progressive, Farmers, or Liberty Mutual is a good option because all of these companies don’t charge more for a longer commute.

When compared to other factors that affect your rates, commute times don’t have much of an impact.

In some states, it could cost as little as $3-$17 per month to move from low or medium coverage to high coverage. Unfortunately, that is not the case in Washington, as you can see in the table below.

| company | Annual Rate with low coverage | Annual Rate with medium coverage | Annual Rate with high coverage |

|---|---|---|---|

| Allstate | $3,340.56 | $3,529.25 | $3,751.75 |

| American Family | $3,514.54 | $3,708.11 | $3,916.41 |

| Farmers | $2,760.41 | $2,963.13 | $3,162.46 |

| Geico | $2,415.05 | $2,570.26 | $2,720.65 |

| Liberty Mutual | $3,755.57 | $4,001.80 | $4,226.82 |

| Nationwide | $2,015.38 | $2,129.08 | $2,245.06 |

| Progressive | $2,916.39 | $3,128.02 | $3,584.15 |

| State Farm | $2,334.70 | $2,510.27 | $2,654.36 |

| USAA | $2,119.91 | $2,260.74 | $2,405.82 |

In nearly every case, Washington auto insurance rates are 6-8 percent higher for medium coverage levels and 11-15 percent higher for high coverage levels.

If your new premium came in the mail with a higher rate, changes in your credit score may be the culprit.

Insurance companies use your credit score (among other information) to judge your likelihood of making a claim.

For most of us, if our credit score drops significantly in a short period of time, it may be due to medical bills, life events such as divorce, or even irresponsible spending habits.

The table below shows each company and their average rates for those with good, fair, and poor credit.

| Company | Annual Rate with Good Credit | Annual Rate with Fair Credit | Annual Rate with Poor Credit |

|---|---|---|---|

| Allstate | $2,877.04 | $3,354.12 | $4,390.41 |

| American Family | $3,177.58 | $3,578.15 | $4,383.33 |

| Farmers | $2,539.95 | $2,726.81 | $3,619.24 |

| Geico | $2,202.06 | $2,446.29 | $3,057.61 |

| Liberty Mutual | $2,758.54 | $3,515.42 | $5,710.24 |

| Nationwide | $1,862.79 | $1,993.82 | $2,532.91 |

| Progressive | $2,935.78 | $3,154.29 | $3,538.50 |

| State Farm | $1,691.05 | $2,177.12 | $3,631.16 |

| USAA | $1,839.15 | $2,092.36 | $2,854.97 |

Based on the percent change from good to fair credit and good to poor credit, It appears that Progressive is the most forgiving in its rates if your credit score suddenly plummets. However, Liberty Mutual and State Farm rates increase the most.

Expect your premium to increase when the unfortunate happens: a speeding ticket, an accident, or a DUI.

| Company | Clean Record | One Speeding Ticket | One Accident | One DUI |

|---|---|---|---|---|

| Allstate | $2,978.15 | $3,331.86 | $3,724.36 | $4,127.71 |

| American Family | $2,978.87 | $3,649.37 | $3,811.59 | $4,412.26 |

| Farmers | $2,454.67 | $3,045.19 | $3,052.21 | $3,295.93 |

| Geico | $1,980.32 | $1,980.32 | $2,534.71 | $3,779.26 |

| Liberty Mutual | $3,409.23 | $3,899.59 | $4,290.97 | $4,379.12 |

| Nationwide | $1,657.44 | $1,811.31 | $2,240.59 | $2,810.03 |

| Progressive | $2,600.49 | $3,138.85 | $4,063.71 | $3,035.03 |

| State Farm | $2,273.58 | $2,499.77 | $2,726.00 | $2,499.77 |

| USAA | $1,664.33 | $1,966.78 | $2,409.13 | $3,008.40 |

Rates increase 10 to 24 percent when you get a speeding ticket; 20 to 56 percent when you get into an accident; and 10 to 91 percent when you get a DUI.

In Washington, it looks like Geico and Nationwide are the most lenient when it comes to speeding tickets. However, State Farm and Progressive are the most lenient when it comes to DUIs.

It’s no surprise that, with any company, an accident mostly guarantees a rate increase.

Enter your ZIP code below to view companies that have cheap auto insurance rates.

Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Your personal information, actions, and preferences most certainly affect your rates, but how Washington regulates auto insurance through laws may also affect your rates.

Let’s take a look.

Auto insurance laws vary from state to state, and Washington is no different.

In this section, we cover more laws associated with auto insurance.

If you are having difficulty purchasing coverage because you have a history of accidents or traffic violations, the Washington Automobile Insurance Plan be a good option.

This plan is provided through a third party company called AIPSO. They collaborate with insurance providers to help at-risk drivers find affordable coverage.

Washington does not have any special low-cost programs for people who don’t have insurance. It is up to you, as the consumer, to shop around for the lowest rate. You can’t afford to NOT have insurance.

Washington Windshield Insurance laws do not require insurance companies to provide windshield repair or replacement, but it is an option, and it is usually covered under comprehensive coverage.

The law does permit insurance companies to use aftermarket and used parts, but you have the option to pay the difference in the quote if you prefer branded materials.

The Washington State Office of the Insurance Commissioner reports on their insurance fraud website that the average U.S. family pays between $400 and $700 annually in increased premiums due to fraudulent acts related to non-health insurance.

For auto insurance, this can come in forms such as overcharging for medical services, staging collisions, or inflating bodily injury claims. Even providing false information to get your insurance quote is a form of fraud.

The Criminal Investigations Unit (CIU) is a division of the Office of the Insurance Commissioner. This unit is responsible for identifying and investigating companies and people who target insurance companies with fraudulent claims. The unit also provides outreach and education about fraud, how to prevent it, and how to report it.

Keep in mind it’s not just policyholders who try to win one over on the insurance companies; doctors, lawyers, and insurance agents could also be involved in fraud.

You can report fraud or suspected fraud on the CIU’s online fraud report page. Don’t let your picture or the picture of someone you know show up on this CIU page.

A statute of limitations is the limit on the amount of time you have, from the time of an accident, to bring a lawsuit to court. Washington permits a lapse of three years from the date and time of the accident to filing.

The only exception is in the case that the driver or a passenger dies after the accident and before the end of the three years. The time is then started from the date of death.

Washington is a “pure comparative fault” state. This means that if you choose to take the at-fault driver to court, and you are partly responsible for the accident, the amount of damages you recover is reduced by the percentage you are at fault.

For instance, if the other driver ran a red light but you also turned right on red when it is prohibited, a judge or jury will decide the percentage of fault each driver had in the accident.

Let’s find out about Washington’s licensing requirements for various populations.

| Young Driver Licensing Laws | Age Restrictions | Passenger Restrictions | Time Restrictions |

|---|---|---|---|

| Learner's Permit | 15 and 6 months or 15 with driver's education | Supervised driving and family members only | 1 a.m. - 5 a.m. (secondarily enforced) |

| Provisional License | 6-month holding period; completion of driver's education if under 18; supervised driving of 50 hours, 10 of which must be at night | First 6 months: no passengers under 20 Second 6 months; no more than 3 passengers under 20 (secondarily enforced) | 1 a.m. - 5 a.m. (secondarily enforced) |

| Full License | 16; completion of driver's education if under 18; with a violation, must wait until 18 | lifted at age 17 | lifted after 12 months or age 18 (minimum age 17) |

| Renewal Procedures | General Population | Older Population |

|---|---|---|

| License renewal cycle | 6 years | 6 years |

| Mail or online renewal permitted | both, every other renewal | not permitted 70 and older |

| Proof of adequate vision required at renewal | every renewal | 70 and older, every renewal |

If you are planning to relocate to Washington, you have a few options. You can apply for a standard driver’s license or an enhanced driver’s license (EDL) which will permit you to re-enter the US by land and sea after traveling to Canada, Mexico, Bermuda, and the Caribbean. However, the EDL has more costly fees, more specific steps, and takes longer to process.

In order to apply for a standard Washington driver’s license, you will need:

Not all Department of Licensing offices administer the written knowledge and driving test.

Knowing some of Washington’s basic driving laws can keep you safe and will help you keep your rates from increasing.

Ready?

Washington drivers must keep right if driving slower than the average speed of surrounding traffic unless passing on the left or turning left.

Washington’s move over laws requires drivers to move out of the lane closest to emergency vehicles and tow trucks. If drivers are unable to move into another lane, they must slow down within 200 feet of the vehicle and are not permitted to speed back up until 200 feet passed the vehicle.

Maximum posted speed limits are 70 mph (60 mph for trucks) on rural interstates, 60 mph on urban interstates, 60 mph on limited-access roads, and 60 mph on all other roads. Some rural interstates may have 75 mph speed limits posted if based on a traffic and engineering study.

Seatbelt laws apply to anyone over the age of 16 in all seats. This law is primarily enforced, and the first offense fine for not using a seatbelt is $124.

Effective January 1, 2020, there are new child safety seat laws in Washington for usage as shown in the table below.

In failing to obey these laws, you could be fined $124, or worse, put your child in danger.

| Washington Child Safety Seat Laws | Rear-facing | Forward-facing with harness | Booster seat | Adult belt |

|---|---|---|---|---|

| Age | younger than 2 | younger than 4 | older than 4 | younger than 16; 12 years and younger must be in the rear seat if practical; 4 and older if in a seating position where there is only a lap belt available |

| Weight | as directed by manufacturer | as directed by manufacturer | N/A | N/A |

| Height | as directed by manufacturer | as directed by manufacturer | shorter than 4 foot 9 inches | taller than 4 foot 9 inches |

Washington is one of 20 states that does not regulate riding in cargo areas of trucks based on age and/or situation.

Rideshare services like Uber require that all their drivers maintain their own auto insurance policies that meet at least the minimum coverages required by Washington law. However, if a driver wishes to obtain special coverage for this role, five companies offer specialized rideshare coverage: Allstate, Metlife, Metromile, State Farm, and USAA.

According to the Insurance Institute for Highway Safety (IIHS), “automation is the use of a machine or technology to perform a task or function that was previously carried out by a human. In driving, automation involves using radar, camera and other sensors to gather information about a vehicle’s surroundings, which is then used by computer programs to perform parts or all of the driving task on a sustained basis.”

Currently, Washington is testing automated vehicles per a June 2017 executive order. An operator is not required to be in the vehicle, but if there is an operator in the vehicle, he or she must be licensed and carry liability insurance.

The two basic practices to ensure your safety and the safety of others is buckling up and obeying the speed limits. Additionally, other laws exist to prevent reckless or impaired driving.

The first through the fourth offense of drinking under the influence in Washington are considered misdemeanors. A fifth violation is considered a felony. The lookback period is seven years.

| Penalty | First Offense | Second Offense | Third Offense | Fourth and Subsequent Offenses |

|---|---|---|---|---|

| License Suspension | 90 days | 2 years | 3 years | same as 3rd |

| Imprisonment | 24 consecutive hours - 365 days OR 15 days electronic home monitoring | 30 days - 365 days, 60 days mandatory electronic home monitoring | 90 days - 365 days, 120 days mandatory electronic home monitoring | same as 3rd |

| Fine | $865.50-$5000 | $1,195.50-$5000 | $2,045.50-$5000 | same as 3rd |

| Other | IID 1 year, addiction education or treatment as ordered | IID 5 years, addiction education or treatment as ordered | IID 10 years, addiction education or treatment as ordered | same as 3rd |

Washington is one of only 10 states that require a treatment and/or prevention education program after the first offense.

The state of Washington was one of the first states to legalize recreational use of marijuana in 2012. Currently, it is illegal for those 21 and older to drive with 5 or more nanograms per milliliter of THC in the blood. The blood test can be performed at a police station or medical facility.

Some 2014 survey and focus group participants in Washington reported that they believed marijuana use improved their driving, but the data says otherwise.

Legal sales began in July of 2014, and results from roadside surveys conducted in Washington are shown in the table below.

| Washington Data | Immediately prior to July 2014 | 6 months following July 2014 | 12 months following July 2014 |

|---|---|---|---|

| Proportion of THC-positive drivers | 14.6% | 19.4% | 21.4% |

Other data comes from an extensive report published by The Governors Highway Safety Association in April 2017.

| Washington Data | 2009-2012 | 2013 | 2014 | First four months of 2015 |

|---|---|---|---|---|

| Percent of impaired driving cases that tested positive for THC | 19.1% | 24.9% | 28% | 33% |

| Washington Data | 2005 | 2014 |

|---|---|---|

| THC positive collisions and DUI arrests (excluding alcohol) | 20% | 30% |

| Median THC levels | 4.0 nanograms per milliliter of blood | 5.6 nanograms per milliliter of blood |

| Washington Data | 2010 | 2013 | 2014 |

|---|---|---|---|

| Number of drivers involved in fatal crashes who had a detectable concentration of THC in their blood | 48 | 49 | 106 |

| Proportion of drivers involved in fatal crashes who had a detectable concentration of THC in their blood | 7.9% | 8.3% | 17% |

| Percent of drivers positive for cannabinoids were also positive for THC | 44.4% | N/A | 84.3% |

| Number of drivers involved in fatal crashes who had THC levels higher than 5 ng/mL | N/A | N/A | 38 of 75 |

The report also described experimental studies that found marijuana affects “psychomotor skills and cognitive functions associated with driving, including vigilance, time and distance perception, lane tracking, motor coordination, divided attention tasks, and reaction time.”

Watch this news report to understand a bit more about driving while under the influence of marijuana.

The best way to safely operate a motor vehicle without taking the chance of being issued a DUI is to avoid recreational use of marijuana all together because it is difficult to determine your ng/mL based on how high you feel. There’s always Uber or Lyft.

However, the Washington State Liquor and Cannabis Board provides guidance to cannabis users who plan to drive.

Published research says, for some people, after using marijuana, it can take up to three hours for THC levels to drop below 5 ng/ml. It could take longer depending on body size and gender.

A nanogram is one-billionth of a gram. A gram is about 1/30 of an ounce, but the way an individual metabolizes THC can vary. The Board reports that some people may still exhibit impaired behavior with less than five ng/ml of THC in their blood.

The Board encourages marijuana smokers or vapors to wait at least five hours before getting behind the wheel and recommends those who use marijuana edibles to wait 10 hours because it can remain in your system much longer.

Unfortunately, in a 2014 Washington roadside survey conducted by the Pacific Institute for Research & Evaluation, 44 percent of the drivers reported that they had driven within two hours of using marijuana in the past year.

Many states have distracted driving laws; some are vague like “no texting” while others are more specific. Washington has extremely specific laws. Because they are so specific, we can make the assumption that texting is banned for all drivers.

Basically, drivers can be cited for engaging in any activity not related to the operation of the vehicle if it makes them a more dangerous driver.

Drivers are prohibited from holding any type of personal electronic device or using a finger to interact with a device. The exception is one-touch activation of an app or function.

Also, don’t be tempted to check your email or text messages while in traffic or at a stoplight. Effective July 2017, you are not permitted to touch your device even while stationary on a public highway.

How safe is it to drive in Washington?

Well, the data our researchers found might surprise you.

Let’s examine the statistics of theft and fatalities from risky driving behavior.

Here are the top 10 stolen cars in Washington:

| Vehicle | Total Thefts (2016) |

|---|---|

| Honda Accord | 3,757 |

| Honda Civic | 3,113 |

| Ford Pickup (Full Size) | 745 |

| Acura Integra | 640 |

| Toyota Camry | 602 |

| Subaru Legacy | 599 |

| Chevrolet Pickup (Full Size) | 562 |

| Jeep Cherokee/Grand Cherokee | 362 |

| Toyota Corolla | 332 |

| Nissan Sentra | 296 |

Listed below are the 10 cities in which the most vehicles were stolen in 2013.

| City | Number of Vehicle Thefts |

|---|---|

| Seattle | 4,310 |

| Spokane | 2,290 |

| Tacoma | 2,024 |

| Everett | 1,034 |

| Vancouver | 976 |

| Kent | 870 |

| Federal Way | 764 |

| Renton | 683 |

| Auburn | 672 |

| Yakima | 594 |

Keeping your eyes on the road and being alert and aware of common risky driving problems in your state is the best way to stay safe.

Let’s look at the data a little more closely.

| Weather Condition | Daylight | Dark, but Lighted | Dark | Dawn or Dusk | Other / Unknown | Total |

|---|---|---|---|---|---|---|

| Normal | 198 | 88 | 88 | 28 | 1 | 403 |

| Rain | 27 | 16 | 17 | 1 | 0 | 61 |

| Snow/Sleet | 6 | 4 | 5 | 1 | 0 | 16 |

| Other | 2 | 3 | 7 | 0 | 1 | 13 |

| Unknown | 15 | 9 | 13 | 2 | 4 | 43 |

| TOTAL | 248 | 120 | 130 | 32 | 6 | 536 |

| Type | Number of Fatalities |

|---|---|

| Traffic Fatalities | 565 |

| Passenger Vehicle Occupant Fatalities (All Seat Positions) | 345 |

| Motorcyclist Fatalities | 80 |

| Drivers Involved in Fatal Crashes | 817 |

| Pedestrian Fatalities | 103 |

| Bicyclist and other Cyclist Fatalities | 14 |

| Person Type | Number |

|---|---|

| Occupants (Enclosed Vehicles) | 64 |

| Motorcyclists | 14 |

| Nonoccupants | 22 |

| Crash Type | Number |

|---|---|

| Single Vehicle | 340 |

| Involving a Large Truck | 77 |

| Involving Speeding | 172 |

| Involving a Rollover | 101 |

| Involving a Roadway Departure | 306 |

| Involving an Intersection (or Intersection Related) | 122 |

| County | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| King County | 80 | 83 | 109 | 100 | 111 |

| Pierce County | 42 | 48 | 66 | 73 | 57 |

| Yakima County | 24 | 35 | 35 | 30 | 48 |

| Snohomish County | 32 | 33 | 53 | 44 | 42 |

| Spokane County | 36 | 29 | 36 | 26 | 41 |

| Clark County | 20 | 35 | 24 | 20 | 28 |

| Whatcom County | 18 | 15 | 11 | 12 | 25 |

| Thurston County | 14 | 15 | 14 | 17 | 19 |

| Kitsap County | 8 | 16 | 18 | 21 | 17 |

| Grant County | 24 | 13 | 17 | 19 | 16 |

| Top Ten Counties | 304 | 322 | 386 | 374 | 404 |

| All Other Counties | 132 | 140 | 165 | 162 | 161 |

| All Counties | 436 | 462 | 551 | 536 | 565 |

| County | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| Adams | 1 | 1 | 4 | 0 | 4 |

| Asotin | 0 | 0 | 1 | 0 | 0 |

| Benton | 2 | 1 | 0 | 7 | 4 |

| Chelan | 3 | 2 | 2 | 1 | 0 |

| Clallam | 0 | 1 | 0 | 1 | 0 |

| Clark | 13 | 10 | 7 | 4 | 9 |

| Columbia | 0 | 0 | 1 | 0 | 0 |

| Cowlitz | 8 | 2 | 1 | 3 | 4 |

| Douglas | 1 | 2 | 0 | 2 | 0 |

| Ferry | 1 | 0 | 2 | 1 | 1 |

| Franklin | 1 | 5 | 1 | 4 | 1 |

| Garfield | 0 | 0 | 0 | 0 | 1 |

| Grant | 6 | 1 | 4 | 5 | 4 |

| Grays Harbor | 1 | 1 | 2 | 1 | 3 |

| Island | 1 | 0 | 3 | 1 | 2 |

| Jefferson | 1 | 1 | 1 | 0 | 0 |

| King | 30 | 38 | 37 | 30 | 41 |

| Kitsap | 8 | 9 | 9 | 7 | 5 |

| Kittitas | 1 | 1 | 2 | 4 | 3 |

| Klickitat | 2 | 0 | 0 | 1 | 1 |

| Lewis | 3 | 1 | 1 | 3 | 2 |

| Lincoln | 1 | 1 | 0 | 1 | 0 |

| Mason | 0 | 4 | 1 | 5 | 1 |

| Okanogan | 2 | 3 | 4 | 2 | 1 |

| Pacific | 1 | 0 | 0 | 2 | 0 |

| Pend Oreille | 5 | 2 | 2 | 2 | 1 |

| Pierce | 26 | 17 | 22 | 19 | 22 |

| San Juan | 0 | 0 | 1 | 0 | 0 |

| Skagit | 5 | 6 | 3 | 1 | 3 |

| Skamania | 0 | 2 | 2 | 0 | 1 |

| Snohomish | 17 | 13 | 14 | 16 | 17 |

| Spokane | 10 | 7 | 5 | 5 | 10 |

| Stevens | 2 | 4 | 3 | 1 | 2 |

| Thurston | 7 | 7 | 7 | 6 | 5 |

| Wahkiakum | 0 | 0 | 0 | 1 | 0 |

| Walla Walla | 0 | 3 | 0 | 0 | 1 |

| Whatcom | 12 | 4 | 4 | 6 | 12 |

| Whitman | 2 | 2 | 3 | 3 | 1 |

| Yakima | 11 | 11 | 8 | 9 | 10 |

| County | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| Adams | 0 | 0 | 1 | 1 | 2 |

| Asotin | 0 | 0 | 1 | 2 | 0 |

| Benton | 1 | 3 | 3 | 8 | 5 |

| Chelan | 2 | 1 | 1 | 2 | 0 |

| Clallam | 2 | 2 | 0 | 5 | 2 |

| Clark | 9 | 10 | 8 | 6 | 8 |

| Columbia | 0 | 0 | 0 | 0 | 0 |

| Cowlitz | 5 | 1 | 3 | 1 | 2 |

| Douglas | 1 | 2 | 0 | 2 | 1 |

| Ferry | 2 | 1 | 1 | 2 | 0 |

| Franklin | 2 | 3 | 1 | 1 | 4 |

| Garfield | 0 | 0 | 0 | 0 | 1 |

| Grant | 6 | 4 | 5 | 7 | 5 |

| Grays Harbor | 2 | 1 | 0 | 2 | 2 |

| Island | 1 | 0 | 3 | 0 | 2 |

| Jefferson | 0 | 1 | 1 | 1 | 0 |

| King | 31 | 27 | 31 | 25 | 41 |

| Kitsap | 4 | 4 | 4 | 4 | 4 |

| Kittitas | 1 | 0 | 4 | 2 | 2 |

| Klickitat | 1 | 1 | 0 | 0 | 0 |

| Lewis | 4 | 2 | 4 | 2 | 4 |

| Lincoln | 0 | 0 | 0 | 1 | 1 |

| Mason | 2 | 2 | 3 | 4 | 2 |

| Okanogan | 2 | 6 | 3 | 3 | 3 |

| Pacific | 1 | 0 | 0 | 2 | 0 |

| Pend Oreille | 2 | 2 | 2 | 2 | 1 |

| Pierce | 22 | 15 | 15 | 26 | 21 |

| San Juan | 0 | 1 | 1 | 0 | 0 |

| Skagit | 3 | 5 | 4 | 1 | 4 |

| Skamania | 0 | 1 | 5 | 0 | 1 |

| Snohomish | 11 | 3 | 14 | 13 | 10 |

| Spokane | 10 | 10 | 13 | 11 | 9 |

| Stevens | 4 | 2 | 2 | 2 | 3 |

| Thurston | 2 | 3 | 4 | 6 | 6 |

| Wahkiakum | 0 | 0 | 0 | 1 | 0 |

| Walla Walla | 1 | 2 | 1 | 2 | 1 |

| Whatcom | 4 | 4 | 1 | 3 | 8 |

| Whitman | 0 | 0 | 1 | 2 | 2 |

| Yakima | 13 | 14 | 7 | 10 | 21 |

| Teens and Drunk Driving | Data |

|---|---|

| Alcohol-Impaired Driving Fatalities Per 100K Population | 1.3 |

| Higher/Lower Than National Average (1.2) | higher |

| DUI Arrest (Under 18 years old) | 121 |

| Rank in US | 29th |

| DUI Arrests (Under 18 years old) Total Per Million People | 74.26 |

As shown in the table above, compared to other states, Washington is ranked 29th in the nation for most teens per million who have been arrested for a DUI.

However, the fatality rate of teens who drink and drive is slightly higher than the national average.

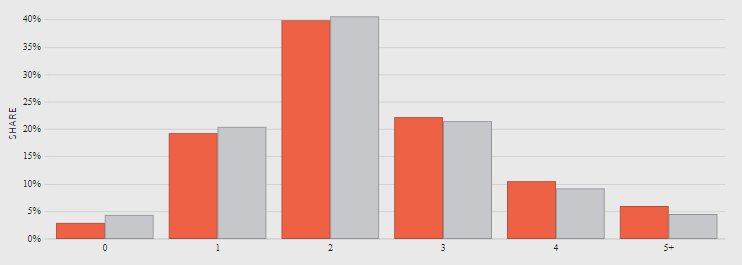

If you live in Washington, chances are you live in a two to three-car household, drive alone to work, and spend 10-34 minutes commuting.

Based on 2017 data, the largest share of households in Washington (red) has 2 cars, followed by 3 cars and is very similar to the national average (gray).

With an average commute time of 26.1 minutes, Washington ranked above the national average of 25.3 minutes in 2017.

That means 3.01 percent of Washington residents suffer through a “super commute” spending in excess of 90 minutes in the car.

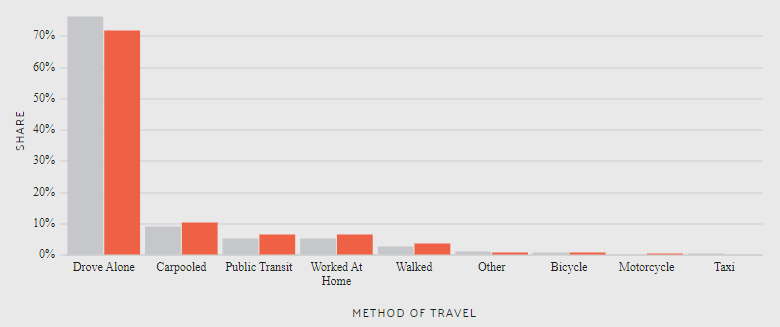

Most people in Washington drive to work alone.

Traffic is likely a bother since 84 percent of Washington residents live in urban areas.

According to the INRIX Scorecard, Seatle ranked 6th in the US for worst traffic. Those who drive in Seattle sit in traffic for 138 hours per year. This time spent in congestion equates to $1,932 per driver.

During peak commute times in Seattle, the average speed is just under 22 mph. During off-peak times, the average speed is just over 39 mph.

Once you get out of traffic and to your destination, start comparison shopping auto insurance rates today.

Auto Insurance Company Reviews / States