8:00 - 17:00

Opening Hour: Mon - Fri

Choosing the right auto insurance company can be overwhelming when there are so many options to choose from.

Finding the quality car insurance company that’s right for you doesn’t have to be as hard as you think. In fact, it can be quite simple.

We’ll take you step-by-step through the process and show you how to confidently choose the right car insurance company for your situation.

You can compare car insurance quotes right here using our free quote tool!

Here’s what we cover:

Table of Contents

Knowing what you’re looking for is the place to start. Each state requires car insurance coverage at a different level, but what the mandatory coverage has in common between states is that it covers your liability and not your own vehicle damage costs.

The minimum you’re required to carry is known as “basic coverage” or “state minimum.”

Considering that most states require significantly less coverage than necessary to pay for the total loss of a new vehicle, you should consider purchasing higher limits even if you decide to only purchase liability coverage.

Without increased liability limits, you’ll have to make up the difference out of pocket between your coverage limit and the cost of the damage you cause.

If your car is financed, you’ll probably be required to carry full coverage insurance. Full coverage includes comprehensive and collision which will offer financial protection for a wide variety of damage to your own vehicle.

If you own your vehicle you can decide if you want to purchase full coverage. If your vehicle is valuable and you wouldn’t be able to recover from its loss out of pocket, you should probably carry full coverage.

There are several coverage types some of which are required depending on where you live, and some of which are optional.

| Type of Coverage | Required or Optional |

|---|---|

| Liability | Required |

| Collision | Owned Vehicle: Optional Leased or Financed Vehicle: Required |

| Comprehensive | Owned Vehicle: Optional Leased or Financed Vehicle: Required |

| Personal Injury Protection (PIP) | Required in some states with "no-fault" laws |

| Medical Payments (MedPay) | Required in some states with "no-fault" laws |

| Uninsured/Underinsured Motorist Coverage | Required in many states |

| Guaranteed Auto Protection (GAP) | Optional |

| Personal Umbrella Policy (PUP) | Optional |

| Rental Reimbursement | Optional |

| Emergency Roadside Assistance | Optional |

| Mechanical Breakdown Insurance | Optional |

| Non-owner Car Insurance | Optional |

| Modified Car Insurance Coverage | Optional |

| Windshield Coverage | Optional |

Related Article: How do I find an affordable auto insurance company?

After you know what you’re looking for, you’re ready to try to find it for less money. Keep reading for tips on how to save as much money as possible!

Car insurance discounts can make a significant difference in your car insurance premiums. Below we’ve charted which providers offer the most discounts as well as the which discounts you may want to ask about when applicable:

| Vehicle Discounts | Driver/Customer Discounts | Personal Discounts |

|---|---|---|

| Active Disabling Device | Claim Free | Emergency Deployment |

| Adaptive Cruise Control | Continuous Coverage | Family Legacy |

| Adaptive Headlights | Defensive Driver | Family Plan |

| Anti-lock Brakes | Driver's Education | Federal Employee |

| Audible Alarm | Driving Device/App | Further Education |

| Automatic Braking | Early Signing | Good Student |

| Blind Spot Warning | Full Payment | Homeowner |

| Daytime Running Lights | Good Credit | Life Insurance |

| Economy Vehicle | Loyalty | Married |

| Electronic Stability Control | Multiple Policies | Membership/Group |

| Farm/Ranch Vehicle | Multiple Vehicles | Military |

| Forward Collision Warning | New Customer/New Plan | New Address |

| Garaging/Storing | Occasional Operator | New Graduate |

| Green/Hyrbid Vehicle | Online Shopper | Non-smoker/Non-drinker |

| Lane Departure Warning | On-time Payments | Occupation |

| Newer Vehicle | Paperless/Auto Billing | Recent Retirees |

| Passive Restraint | Paperless Documents | Stable Residence |

| Utility Vehicle | Roadside Assistance | Student Away |

| Vehicle Recovery | Safe Driver | Student or Alumni |

| VIN Etching | Seat Belt Use | Volunteer |

Many insurance providers have special programs. The programs offer perks for their customers.

Some insurance companies offer accident forgiveness as an option. If you choose this option, you can have an accident and not experience rate hikes.

Some companies offer new car replacement if your current vehicle is totaled.

Low-income car insurance programs are offered in some states:

Plus there are a few non-government run programs like Citizens United Reciprocal Exchange (CURE).

Every six months to a year, you should do a car insurance review. Make sure your current levels of protection are what you still want, and if they’re not, make the changes in your search. Review the following aspects of your coverage:

You could get individual quotes from companies one at a time, but it will save you time to do a search with a comparison tool. We have one here that will give you multiple quotes after you enter your information just one time.

You could save a significant amount of money by finding a company that offers lower rates and switching to them.

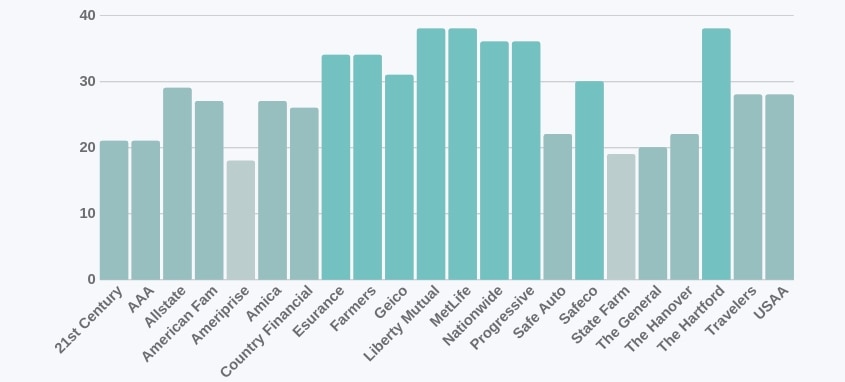

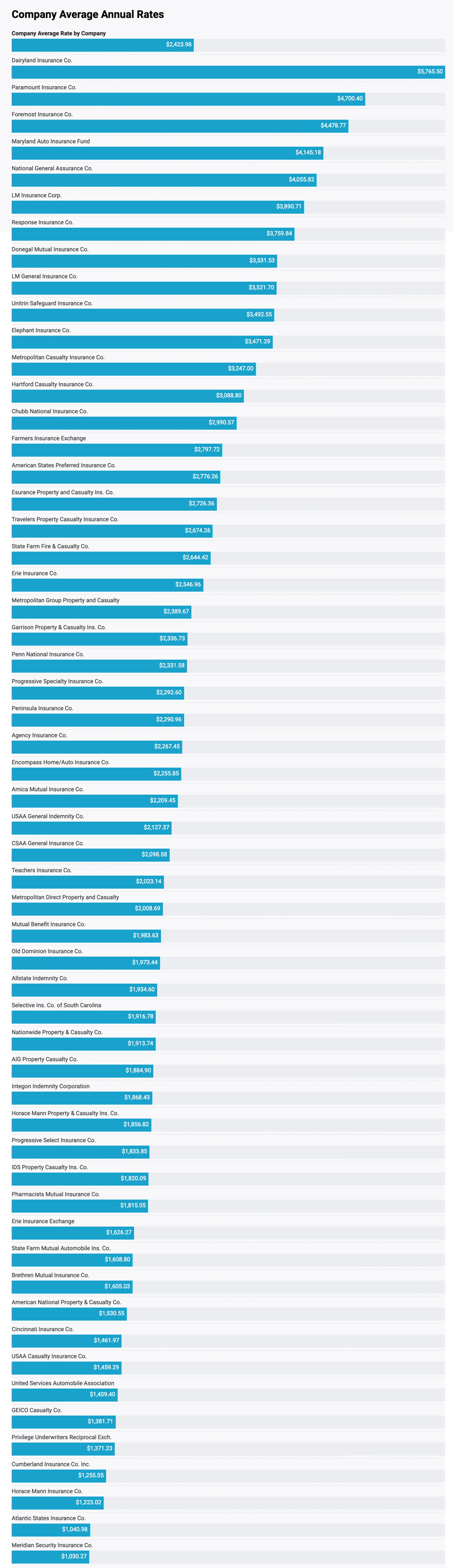

The importance of comparing rates can be understood by reviewing the data we collected from Maryland’s Insurance Department site (see below). Look at the wide span of rates — over a $4,000 difference from most to least expensive.

If you go with the first company you get a quote from you may be costing yourself a lot of money. Check out the car insurance company rates (average annual):

You might be overwhelmed by the different choices of providers. We’ll break down some of the common options so you have an understanding of what you’d prefer.

Now that you understand some of the different types of agents and providers you can choose from, and you’ve compared quotes and found the companies that look best to you, take the next step and do car insurance company research.

We’ll show you where to look below.

When you narrow down the vast list of potential car insurance providers to the top three or four, you’ll need to make sure they’re reputable. Researching to ensure a company’s reputation could save you a headache down the road when you make a claim.

A company that’s not financially stable may be unable to pay your claim. And if a company has poor customer satisfaction results, you may have a negative experience when you have to deal with them over a claim.

If they’re not licensed in your state, it’s an automatic “no” for going with them. If a company isn’t licensed in your state, their coverage won’t be valid.

Check the National Association of Insurance Commissioners (NAIC) search page to see if the companies you’re considering are licensed in your state.

Below, we have listed the websites and phone numbers for each state. You can find accurate information and answers to your questions by contacting your state insurance regulating division.

| States | Website | Phone Number |

|---|---|---|

| Alabama | www.aldoi.gov | (334) 269-3550 |

| Alaska | www.commerce.alaska.gov | 1-800-INSURAK (in-state outside Anchorage) (907) 269-7900 (Anchorage office) (907) 465-2515 (Juneau office) |

| Arizona | https://insurance.az.gov | (602) 364-2499 (800) 325-2548 (In Arizona but outside the Phoenix area) |

| Arkansas | insurance.arkansas.gov | (800) 282-9134 or (501) 371-2600 |

| California | www.insurance.ca.gov | (800) 927-4357 (HELP) (800) 482-4833 (TTY) |

| Colorado | www.colorado.gov/pacific | (303) 894-7855 or (800) 886-7675 |

| Connecticut | www.ct.gov/cid | (860) 297-3800 or (800) 203-3447 |

| Delaware | insurance.delaware.gov | (302) 674-7300 |

| Florida | www.floir.com | (850) 413-3140 |

| Georgia | www.oci.ga.gov | (404) 656-2070 or (800) 656-2298 |

| Hawaii | cca.hawaii.gov/ins | (808) 586-2790 or (808) 586-2799 |

| Idaho | doi.idaho.gov | (208) 334-4250 |

| Illinois | insurance.illinois.gov | (312) 814-2420 (Chicago office) or (217) 782-4515 (Springfield office) |

| Indiana | www.in.gov/idoi | (800) 622-4461 |

| Iowa | iid.iowa.gov | (515) 281-5705 or (877) 955-1212 |

| Kansas | www.ksinsurance.org | (785) 296-3071 or (800) 432-2484 |

| Kentucky | insurance.ky.gov | (800) 595-6053 or (502) 564-3630 |

| Louisiana | www.ldi.la.gov | (800) 259-5300 |

| Maine | www.maine.gov/pfr/insurance | (207) 624-8475 |

| Maryland | http://www.mdinsurance.state.md.us | (410) 468-2090 |

| Massachusetts | www.mass.gov/orgs/division-of-insurance | (617) 521-7794 or (877) 563-4467 |

| Michigan | www.michigan.gov/difs | (517) 284-8800 or (877) 999-6442 |

| Minnesota | mn.gov/commerce | (651) 539-1500 or (800) 657-3602 |

| Mississippi | www.mid.ms.gov | (601) 359-3569 or (800) 562-2957 |

| Missouri | insurance.mo.gov | (573) 751-4126 |

| Montana | https://csimt.gov | (800) 332-6148 or (406) 444-2040 |

| Nebraska | doi.nebraska.gov | (402) 471-2201 |

| Nevada | doi.nv.gov | (888) 872-3234 |

| New Hampshire | www.nh.gov/insurance | (603) 271-2261 or (800) 852-3416 |

| New Jersey | www.state.nj.us/dobi | (609) 292-7272 or (800) 446-7467 |

| New Mexico | www.osi.state.nm.us | (855) 4ASK-OSI (855-427-5674) |

| New York | www.dfs.ny.gov | (800) 342-3736 |

| North Carolina | www.ncdoi.com | (855) 408-1212 |

| North Dakota | www.nd.gov/ndins | (701) 328-2440 or (800) 247-0560 |

| Ohio | www.insurance.ohio.gov | (800) 686-1526 |

| Oklahoma | www.ok.gov/oid | (800) 522-0071 or (405) 5210-2828 |

| Oregon | dfr.oregon.gov | (888) 877-4894 |

| Pennsylvania | www.insurance.pa.gov | (877) 881-6388 |

| Rhode Island | www.dbr.state.ri.us/divisions/insurance | (401) 462-9520 |

| South Carolina | doi.sc.gov | (803) 737-6160 |

| South Dakota | dlr.sd.gov/insurance | (605) 773-3563 |

| Tennessee | www.tn.gov/commerce | (615) 741-2241 |

| Texas | www.tdi.texas.gov | (512) 676-6000 or (800) 578-4677 |

| Utah | insurance.utah.gov | (801) 538-3800 |

| Vermont | www.dfr.vermont.gov | (802) 828-3301 |

| Virginia | www.scc.virginia.gov/boi | (804) 371-9741 or (800) 552-7945 |

| Washington | www.insurance.wa.gov | (800) 562-6900 |

| Washington D.C. | disb.dc.gov | (202) 727-8000 |

| West Virginia | www.wvinsurance.gov | (304) 558-3386 |

| Wisconsin | oci.wi.gov | (608) 266-3585 (Madison) or (800) 236-8517 (statewide) |

| Wyoming | doi.wyo.gov | (307) 777-7401 or (800) 438-5768 |

Some states’ insurance websites make this information readily accessible, such as California’s which displays all the complaint ratio information for the past three years for the top 50 insurance companies. Their ratios are based on the number of justified complaints to 100,000 earned exposures.

Other states’ insurance websites don’t offer the information so easily. The table below lists each state and whether its insurance website offers complaint data (see websites above to access information).

| State | Complaint Info? | State | Complaint Info? | State | Complaint Info? |

|---|---|---|---|---|---|

| Alabama | no | Kentucky | yes | North Dakota | no |

| Alaska | no | Louisiana | no | Ohio | yes |

| Arizona | yes | Maine | yes | Oklahoma | no |

| Arkansas | yes | Maryland | yes | Oregon | yes |

| California | yes | Massachusetts | yes | Pennsylvania | yes |

| Colorado | yes | Michigan | yes | Rhode Island | no |

| Connecticut | yes | Minnesota | no | South Carolina | yes |

| Delaware | no | Mississippi | no | South Dakota | no |

| District of Columbia | no | Missouri | yes | Tennessee | no |

| Florida | yes | Montana | no | Texas | yes |

| Georgia | no | Nebraska | no | Utah | yes |

| Hawaii | yes | Nevada | no | Vermont | no |

| Idaho | yes | New Hampshire | no | Virginia | no |

| Illinois | yes | New Jersey | yes | Washington | yes |

| Indiana | yes | New Mexico | no | West Virginia | yes |

| Iowa | no | New York | yes | Wisconsin | no |

| Kansas | yes | North Carolina | no | Wyoming | yes |

If your state insurance website doesn’t offer complaint information, you can still go to the NAIC’s complaint search and enter the company of your choice to find the number of complaints.

This step is easy. A.M. Best is an independent rating agency. Once you set up your free profile at AMBest.com, you simply enter the company name you’re researching into the search bar to view its grade and outlook.

But, we’ve streamlined the search even more. We’ve compiled the data from A.M. Best for the companies with the best and worst ratings:

| Rating | Outlook | Best Rated Companies | Rating | Outlook | Worst Rated Companies |

|---|---|---|---|---|---|

| A++ | Stable | ACE American Insurance Company | C- | Stable | American Heartland Insurance Company |

| A++ | Stable | Agri General Insurance Company | C | Negative | American Service Insurance Company, Inc. |

| A++ | Stable | Auto-Owners Insurance Company | C+ | Stable | Country-Wide Insurance Company |

| A++ | Stable | Automobile Ins Co of Hartford, CT | C++ | Negative | First Acceptance Insurance Company |

| A++ | Stable | Chubb Insurance Company | C++ | Positive | First Chicago Insurance Company |

| A++ | Stable | Columbia Insurance Company | E | Union Mutual Insurance Company | |

| A++ | Stable | Continental Divide Insurance Company | |||

| A++ | Stable | Geico | |||

| A++ | Stable | Great Northern Insurance Company | |||

| A++ | Stable | Owners Insurance Company | |||

| A++ | Stable | Select Insurance Company | |||

| A++ | Stable | State Farm Mutual Automobile Ins Co | |||

| A++ | Stable | TravCo Insurance Company | |||

| A++ | Stable | The Travelers Companies | |||

| A++ | Stable | United Services Automobile Association |

Like the grades, you got in school, “A’s” are good and “+’s” are even better. You want a company with a good rating and a stable outlook. Find out more about AM Best’s rating here.

Enter your ZIP code below to view companies that have cheap auto insurance rates.

Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

The following independent companies compile mountains of data a year to provide consumers with ratings and recommendations:

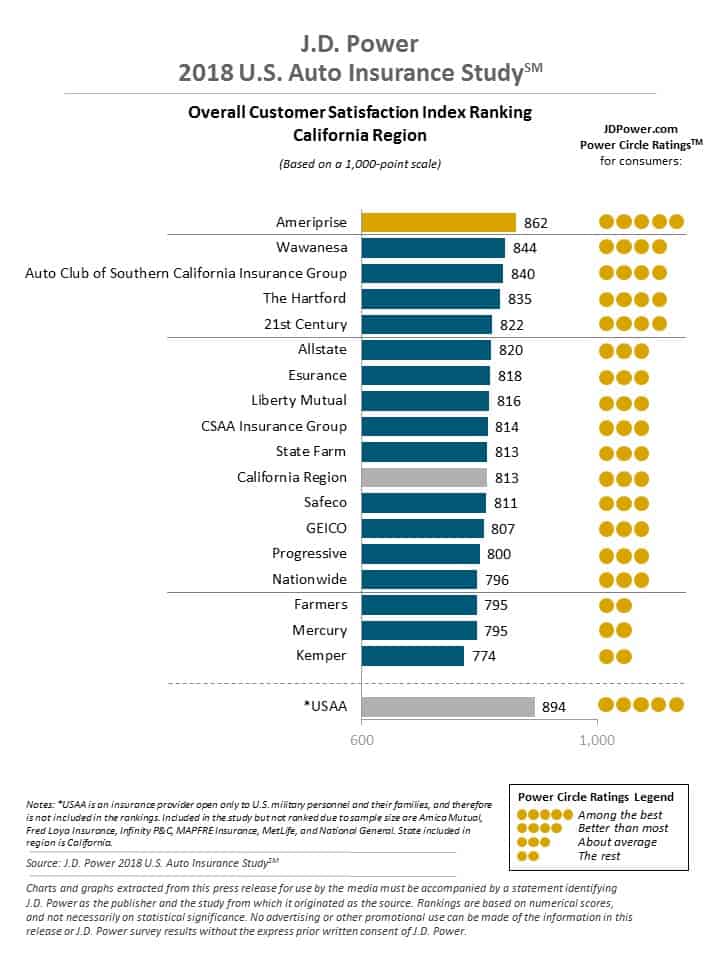

This is a valuable resource. Every year they publish an insurance study and rank the insurance companies in various regions. You can search by region and see the highest and best-rated companies where you live.

They list the top-rated car insurance companies as follows:

You may be familiar with the Consumer Reports magazine and website already. One area they address often is car insurance. See what they have to say about the companies you’re interested in.

Here are Consumer Reports’ ratings for car insurance companies (subscription required to view results on their page):

| Car Insurance Company | Reader Score | Excellentase of Reaching an Agent | Simplicity of the Process | Promptness of Response | Damage Amount | Agent Courtesy | Timely Payment | Freedom to Select Repair Shop | Being Kept Informed of Claim Status |

|---|---|---|---|---|---|---|---|---|---|

| Allstate Insurance Goodroup | 88 | Excellent | Very Good | Very Good | Very Good | Excellent | Excellent | Very Good | Very Good |

| American Family Insurance Goodroup | 89 | Excellent | Very Good | Very Good | Very Good | Excellent | Very Good | Very Good | Excellent |

| Ameriprise P&C Companies | 89 | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good | Good |

| Amica Mutual Insurance Company | 96 | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent |

| Auto Club Excellentnterprises Insurance Goodroup | 92 | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Very Good |

| Auto Club Goodroup | 94 | Excellent | Excellent | Excellent | Very Good | Excellent | Excellent | Very Good | Very Good |

| Auto-Owners Insurance Goodroup | 93 | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Very Good |

| Berkshire Hathaway Insurance Goodroup | 89 | Excellent | Very Good | Excellent | Very Good | Excellent | Excellent | Very Good | Very Good |

| California State Auto Goodroup (CSAA) | 90 | Very Good | Very Good | Very Good | Very Good | Excellent | Excellent | Excellent | Very Good |

| Excellentrie Insurance Goodroup | 94 | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Very Good |

| Farm Bureau Property & Casualty Insurance Company | 90 | Very Good | Very Good | Very Good | Very Good | Excellent | Very Good | Excellent | Very Good |

| Farmers Insurance Goodroup | 89 | Excellent | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good |

| Hanover Insurance Goodroup Property & Casualty Companies | 90 | Excellent | Very Good | Excellent | Very Good | Excellent | Excellent | Excellent | Very Good |

| Hartford Insurance Goodroup | 90 | Excellent | Very Good | Excellent | Very Good | Excellent | Excellent | Excellent | Very Good |

| Liberty Mutual Insurance Companies | 88 | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good |

| MAPFRE North America Group | 86 | Very Good | Very Good | Very Good | Good | Very Good | Very Good | Very Good | Good |

| Mercury Goodeneral Goodroup | 86 | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good | Very Good | Good |

| MetLife Auto & Home Goodroup | 86 | Very Good | Very Good | Very Good | Good | Very Good | Very Good | Very Good | Good |

| Nationwide Goodroup | 88 | Very Good | Very Good | Very Good | Very Good | Excellent | Very Good | Very Good | Very Good |

| NJM Insurance Goodroup | 95 | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Very Good |

| PExcellentMCO Mutual Insurance Company | 93 | Excellent | Excellent | Excellent | - | Excellent | - | - | - |

| Progressive Insurance Goodroup | 87 | Very Good | Very Good | Very Good | Very Good | Very Good | Excellent | Very Good | Very Good |

| State Auto Insurance Companies | 89 | Very Good | Very Good | Very Good | Very Good | Very Good | Excellent | Very Good | Very Good |

| State Farm Goodroup | 89 | Excellent | Very Good | Very Good | Very Good | Excellent | Very Good | Very Good | Excellent |

| The Cincinnati Insurance Company | 93 | Excellent | Excellent | Excellent | - | Excellent | - | - | - |

| Travelers Goodroup | 90 | Excellent | Very Good | Excellent | Very Good | Excellent | Excellent | Excellent | Very Good |

| USAA Goodroup | 95 | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent | Excellent |

While J.D. Power and Consumer Reports will give you general information about car insurance companies as a whole, the BBB grades individual offices. You’ll get the most specific rating for the local office you’re considering from the BBB as opposed to the other rating companies.

Making sure you choose the right car insurance company is well worth the effort. If you need to file a claim, you’ll be glad you chose a company that is financially stable and consumer-friendly.

Now that you know how to choose a car insurance company, you can purchase your coverage from the right car insurance company. Now, it’s time to let them help you understand your policy.

Read on for suggestions of questions to ask:

The NAIC suggests asking these questions of your insurer:

Find your state on the NAIC consumer complaint map to be directed to your state’s website with directions for making a complaint.

Each state makes its own requirements for car insurance. Find your state insurance website on the NAIC map to find out the requirements where you live.

If your vehicle is leased or financed, your lender will likely require full coverage.

As often as you want. But be careful you don’t allow your policy to lapse.

Yes, if the company offers both types. Often you’ll be eligible for a significant discount when you combine your auto policy with a home or rental policy. You could also combine car insurance with a motorcycle or RV policy.

Even insuring a second vehicle with the same insurer could get you a discount.

By doing a car insurance quote comparison. Make sure to review your policy and coverage at least once a year.

Also, we’ve collected the average annual premiums for full coverage in each state (that includes liability, comprehensive, and collision):

| States | 2015 Average Annual Rates | 2014 Average Annual Rates | 2013 Average Annual Rates | 2012 Average Annual Rates | 2011 Average Annual Rates |

|---|---|---|---|---|---|

| Idaho | $679.89 | $673.13 | $650.57 | $639.19 | $641.96 |

| Iowa | $702.46 | $683.67 | $668.09 | $656.84 | $648.99 |

| Maine | $703.82 | $689.12 | $674.94 | $667.66 | $662.28 |

| Wisconsin | $737.18 | $716.83 | $689.77 | $666.79 | $669.99 |

| Indiana | $755.03 | $728.93 | $704.50 | $724.44 | $710.36 |

| Vermont | $764.02 | $746.79 | $734.82 | $726.57 | $716.14 |

| South Dakota | $766.91 | $744.28 | $717.30 | $690.95 | $669.20 |

| North Dakota | $773.30 | $768.09 | $743.27 | $714.75 | $688.74 |

| Ohio | $788.56 | $766.66 | $738.68 | $714.05 | $697.61 |

| North Carolina | $789.09 | $768.28 | $739.91 | $720.47 | $708.10 |

| New Hampshire | $818.75 | $795.50 | $773.30 | $755.76 | $746.57 |

| Nebraska | $831.02 | $805.99 | $773.64 | $751.18 | $732.21 |

| Virginia | $842.67 | $836.14 | $809.40 | $781.38 | $768.95 |

| Wyoming | $847.44 | $844.33 | $804.52 | $796.14 | $791.14 |

| Kansas | $862.93 | $850.79 | $815.82 | $785.72 | $780.43 |

| Montana | $863.52 | $868.55 | $842.74 | $821.68 | $816.21 |

| Alabama | $868.48 | $837.09 | $811.75 | $788.07 | $784.38 |

| Tennessee | $871.43 | $855.56 | $829.38 | $794.53 | $767.82 |

| Missouri | $872.43 | $845.39 | $819.79 | $799.14 | $790.27 |

| Utah | $872.93 | $852.66 | $820.92 | $805.32 | $809.35 |

| Hawaii | $873.28 | $858.16 | $844.16 | $844.12 | $861.95 |

| Minnesota | $875.49 | $856.62 | $823.70 | $800.24 | $777.17 |

| Illinois | $884.56 | $854.10 | $819.27 | $806.21 | $803.04 |

| Oregon | $904.83 | $894.10 | $856.26 | $818.07 | $804.59 |

| Arkansas | $906.34 | $900.18 | $868.13 | $843.07 | $829.13 |

| New Mexico | $937.59 | $920.42 | $888.83 | $866.19 | $869.85 |

| Kentucky | $938.51 | $917.49 | $904.99 | $888.46 | $872.48 |

| Washington | $968.80 | $952.10 | $914.04 | $891.04 | $889.82 |

| Pennsylvania | $970.51 | $950.42 | $930.48 | $915.83 | $904.47 |

| Arizona | $972.85 | $961.88 | $926.52 | $899.91 | $899.33 |

| South Carolina | $973.10 | $936.69 | $904.22 | $880.82 | $857.70 |

| Colorado | $981.64 | $939.52 | $887.57 | $849.74 | $835.50 |

| California | $986.75 | $951.75 | $922.69 | $891.68 | $881.07 |

| Mississippi | $994.05 | $957.59 | $925.13 | $902.95 | $895.69 |

| Oklahoma | z$1,005.32 | $985.58 | $931.41 | $902.90 | $881.50 |

| West Virginia | $1,025.78 | $1,032.45 | $1,021.37 | $1,005.68 | $992.57 |

| Alaska | $1,027.75 | $1,050.09 | $1,058.15 | $1,053.54 | $1,053.48 |

| Georgia | $1,048.40 | $991.25 | $949.33 | $922.05 | $912.49 |

| Nevada | $1,103.05 | $1,083.42 | $1,047.74 | $1,024.09 | $1,029.87 |

| Texas | $1,109.66 | $1,066.20 | $1,017.81 | $974.68 | $959.87 |

| Maryland | $1,116.45 | $1,096.37 | $1,071.35 | $1,056.82 | $1,048.86 |

| Massachusetts | $1,129.29 | $1,107.76 | $1,080.48 | $1,048.06 | $1,011.14 |

| Connecticut | $1,151.07 | $1,132.78 | $1,109.03 | $1,082.28 | $1,068.18 |

| Delaware | $1,240.57 | $1,215.69 | $1,187.18 | $1,153.59 | $1,134.60 |

| Florida | $1,257.13 | $1,208.77 | $1,209.70 | $1,196.57 | $1,160.13 |

| Rhode Island | $1,303.50 | $1,257.40 | $1,210.55 | $1,176.05 | $1,148.97 |

| District of Columbia | $1,330.73 | $1,324.39 | $1,316.48 | $1,289.49 | $1,276.99 |

| New York | $1,360.66 | $1,327.82 | $1,301.49 | $1,273.70 | $1,236.77 |

| Michigan | $1,364.00 | $1,350.58 | $1,264.20 | $1,171.94 | $1,110.64 |

| New Jersey | $1,382.79 | $1,379.20 | $1,369.70 | $1,334.59 | $1,303.52 |

| Louisiana | $1,405.36 | $1,364.17 | $1,307.72 | $1,275.10 | $1,281.55 |

| U.S. Average | $1,009.38 | $981.77 | $950.92 | $924.45 | $908.43 |

Get Your Rates Quote Now |

|||||

Choosing the right car insurance company is worth the effort.

Get started comparing quotes from multiple providers at once using our free rate tool. Enter your zip code below to get started!

Auto Insurance Company Reviews / Auto Insurance Tips