8:00 - 17:00

Opening Hour: Mon - Fri

| Louisiana Statistics Summary | Details |

|---|---|

| Road Miles in State | 48,252 |

| Number of Vehicles Registered | 3,772,692 |

| Population | 4,659,978 |

| Most popular vehicle | F150 |

| Uninsured % | 13% |

| Total Driving Related Deaths | Speeding: 177 DUI: 225 |

| Full Coverage Annual Premiums | Liability: $775.83 Collision: $414.36 Comprehensive: $215.17 |

| Cheapest Providers | USAA and State Farm |

The fact that Louisiana has astronomical auto insurance rates is old news… so old, the reasons date back over 100 years.

Insurance companies and lawmakers have been joining forces the best they know-how over the last several decades, but rates still struggle to approach reasonable by comparison to other states.

There can’t be a quick fix overnight, but if Louisiana residents are at least made aware of the causes behind the high auto insurance rates and the options in reducing them as much as possible, there may be hope in fitting your annual premium into your budget.

We cover rates, laws, and explanations of factors that can increase or lower your rate quotes with the top-five insurance companies in Louisiana.

So, pull up a chair and get ready!

Guess what…comparing rates is a great way to put money back into your pocket with big, big savings! Start today with just your ZIP code.

Table of Contents

Before we get into all the details, we need to be open, honest, and clear.

Louisiana has one of the highest auto insurance rates in the country.

We will get into more about why the rates are so high a little later on. For now, let’s get started with the basics of how much you could expect to pay for auto insurance in Louisiana.

| Insurance Required | Limits |

|---|---|

| Bodily injury coverage | $15,000 per person $30,000 per accident |

| Property damage coverage | $25,000 |

Liability auto insurance coverage pays anyone owed compensation when there is an accident you caused.

Louisiana is an “at-fault” state, which means if an accident was your fault, you (or your insurance company) is responsible for all of the damages.

Louisiana requires that you carry, at the minimum, the following amounts:

Remember, these are the minimum coverage for auto insurance in Louisiana and do not cover injury, death, or damage to yourself or your own passengers!

The state of Louisiana requires proof of minimum liability coverage prior to registering a vehicle, according to its official website. Beyond that point, it is the responsibility of the driver to continue liability coverage and carry proof of coverage.

If you are pulled over or you are in an accident, and you do not have a way to prove you’re insured, a police officer will issue you a violation. You will then have three days to show proof of insurance at an OMV location.

If you fail to provide proof of minimum liability coverage within three days, you will incur fees, your license plate will be confiscated, and you will have to re-register your vehicle.

Be sure to always carry proof of insurance, and it wouldn’t hurt to have a copy of the Safety Responsibility Claim Form if you are in an accident with someone who does not have proof of insurance.

How exactly affordable is auto insurance for Louisiana residents?

Let’s find out.

In 2014, the annual per capita disposable personal income in Louisiana was $37,787.

Disposable personal income (DPI) is the total amount of money available for an individual to spend (or save) after their taxes have been paid.

The average annual cost of auto insurance in Louisiana is $1,364.

Unfortunately, Louisiana residents pay one of the largest percents of of their income on their annual auto insurance premium in the nation (second to Michigan). Louisiana residents pay almost four percent annually of their average DPI.

The average Louisiana resident has $3,148 each month for living expenses. Auto insurance alone will cost about $125.

Why is getting the best deal on auto insurance so important?

American Consumer Credit Counseling suggests saving 20 percent of every paycheck. With Louisiana’s DPI, that’s about $630 each month! How much are you contributing to your nest egg each month?

| Coverage Types | Average Annual Auto Insurance Rates |

|---|---|

| Liability | $775.83 |

| Collision | $414.36 |

| Comprehensive | $215.17 |

| Full Coverage | $1,405.36 |

Worth noting, the state of Louisiana has THE highest full coverage rates in the nation as of 2015!

The national average of all states for full coverage is $1,009.38. You can see Louisiana comes in over $400 higher than the national average.

Louisiana also fell within the top eight states with the highest coverage rates for liability, collision, and comprehensive in 2015.

Let that sink in…

Now, before we go blaming it all on Mardi Gras, let’s take a deep breath and look at the finite details.

Just because your state has the highest rates in the nation does not mean you can’t get a reasonable deal on an auto insurance policy.

What’s the good news?

You have the opportunity to shop diligently for excellent coverage for a great rate. Keep reading to learn more about the different types of auto insurance coverage.

Even though Louisiana has minimum requirements for liability coverage, experts recommend drivers purchase more. The state’s minimum amounts don’t even come close to the bills to expect if you are at fault for an accident.

You may be wondering: Why do I need more coverage than required?

Let’s talk about profits and losses for a moment…

When you consider various auto insurance providers, it’s important to look at data on a state level. All insurance companies in the state of Louisiana have what is called a loss ratio per company. We have included the total loss ratio for all insurance providers by coverage type in the state in the table below.

| Loss Ratio | 2013 | 2014 | 2015 |

|---|---|---|---|

| Medical Payments (Med Pay) | 85.88 | 85.62 | 86.66 |

| Uninsured/Underinsured Motorist | 92.10 | 100.11 | 99.68 |

A loss ratio shows how much a company spends on the types of claims to how much money they take in on premiums. A loss ratio of 60 percent indicates the company spent $60 on claims out of every $100 earned in premiums.

So, the closer the ratio is to 100, the more claims that are paid; however, this also shows that insurance companies are losing money. Sixty to 70 loss ratio is considered to be in the safe zone.

Remember, Louisiana is ranked 20th in the nation for the highest percentage of uninsured motorists, so, it makes complete sense that insurance companies are losing money when paying out claims of this type.

And the cycle continues… the more the companies have to pay out on claims, the higher the rates go. The higher the rates go, the more people there are who take a risk and not purchase auto insurance.

Uninsured/underinsured motorists coverage has various options in limits of coverage as well, but, essentially, this type of policy will cover you if you are hit by an uninsured or underinsured motorist.

At 13 percent, Louisiana ranks number 20 out of all 50 states for the highest percentage of uninsured/underinsured motorists.

That is nearly 606,000 people driving around the state of Louisiana without any or enough liability coverage.

Louisiana does not currently require uninsured/underinsured motorists coverage, but it is something to closely consider when purchasing your auto insurance policy.

Insurance companies in Louisiana are required to offer this type of coverage to you, but you do have the option to decline it by providing a written and signed statement that you decline this type of coverage.

You may be wondering, why would I need to submit that in writing?

Well, your insurance company will keep your declination on file in case you are in a no-fault accident with another person who was negligent enough not to follow the laws.

If you choose to purchase uninsured/underinsured motorists coverage, it is required that the amount equal that of your liability coverage.

However, there is another option to keep your rates low: it’s called “economic-only” coverage.

Taking this “economic-only” option will reduce the uninsured motorist coverage below that of your own liability coverage, and, in turn, reduce your premium… but you still have to sign a statement that you are electing for “economic-only” uninsured/underinsured motorist coverage.

We will explain a bit more about this “economic-only” option later on in the driving laws section.

So, unless you want your insurance company to leave you high and dry when a stroke of bad luck collides with you or your vehicle, don’t sign and decline their offer.

We know getting the complete coverage you need for an affordable price is your goal.

The great news is that there are lots of powerful but cheap extras you can add to your policy.

Don’t get overtaken by high auto insurance premiums! Start comparison shopping today using our FREE online tool. Enter your ZIP code below to get started!

Here’s a list of other useful coverage available to you in Louisiana:

Most are under the impression that men pay higher rates than women, and that is true in most cases in Louisiana. However, six states, most recently California, have outlawed charging different insurance rates based on gender and/or marital status.

Our researchers found that the two most influential factors that go into rate calculations are age and the specific carrier.

Let’s see how that shakes out for Louisiana residents.

Many factors go into calculating your rate, not just age, gender, and marital status. We provide a table below featuring average rates for the top five carriers in Louisiana to give you an idea of how these few variables affect rates. Click on the arrows for each column to sort rates.

| Company | Married 35-year-old Female Annual Rate | Married 35-year-old Male Annual Rate | Married 60-year-old Female Annual Rate | Married 60-year-old Male Annual Rate | Single 25-year-old Female Annual Rate | Single 25-year-old Male Annual Rate | Single 17-year-old Female Annual Rate | Single 17-year-old Male Annual Rate | Average Rate (over 17) Annual Rate | Average Rate (17-year-olds) Annual Rate | The Difference |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Allstate | $4,254.40 | $4,254.40 | $4,394.91 | $4,394.91 | $4,694.46 | $5,083.73 | $9,256.33 | $11,657.16 | $4,512.80 | $10,456.75 | $5,943.94 |

| Geico | $3,430.68 | $3,952.72 | $4,103.66 | $5,009.51 | $3,309.53 | $3,204.45 | $12,767.36 | $13,458.88 | $3,835.09 | $13,113.12 | $9,278.03 |

| Progressive | $4,158.02 | $3,880.90 | $3,483.46 | $3,762.32 | $4,746.19 | $4,834.20 | $16,529.91 | $18,373.77 | $4,144.18 | $17,451.84 | $13,307.66 |

| State Farm | $2,851.05 | $2,851.05 | $2,619.17 | $2,619.17 | $3,180.57 | $3,569.11 | $8,404.12 | $10,538.72 | $2,948.35 | $9,471.42 | $6,523.07 |

| USAA | $2,678.38 | $2,634.64 | $2,612.63 | $2,591.11 | $3,286.33 | $3,597.39 | $8,021.04 | $9,403.41 | $2,900.08 | $8,712.23 | $5,812.15 |

You will notice three columns at the far right of the table that shows the average rate for those over 17 compared to those age 17. Age is an acceptable factor in calculating rates; after all, the older we are, the more experience we have as drivers.

But it also has a great deal to do with risky behavior and how the statistics come out for younger drivers.

The Insurance Institute for Highway Safety (IIHS) released an informative video not too long ago that explains why insurance rates are so high for teens.

Another factor that influences rate calculations is where you live.

Statistically, the more populated an area is, the more risk you will be for having an accident not to mention DUI rates statewide and many other risk factors.

We include in the tables below the average rate by ZIP code. Feel free to search the tables for your ZIP code and maybe cities to which you plan to relocate.

| Cheapest ZIP Codes in Louisiana | City | Average Annual Rate by ZIP Codes | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|---|

| 71001 | ARCADIA | $4,604.07 | Allstate | $5,413.73 | Progressive | $5,206.83 | State Farm | $3,594.95 | USAA | $3,758.45 |

| 71016 | CASTOR | $4,592.82 | Allstate | $5,413.73 | Progressive | $5,270.63 | State Farm | $3,553.73 | USAA | $3,843.04 |

| 71038 | HAYNESVILLE | $4,630.28 | Progressive | $5,439.25 | Allstate | $5,413.73 | State Farm | $3,577.56 | USAA | $3,645.13 |

| 71045 | JAMESTOWN | $4,608.94 | Allstate | $5,413.73 | Progressive | $5,270.63 | State Farm | $3,634.33 | USAA | $3,843.04 |

| 71048 | LISBON | $4,601.27 | Allstate | $5,413.73 | Progressive | $5,298.84 | State Farm | $3,624.07 | USAA | $3,645.13 |

| 71068 | RINGGOLD | $4,613.19 | Allstate | $5,413.73 | Progressive | $5,216.23 | State Farm | $3,709.97 | USAA | $3,843.04 |

| 71071 | SAREPTA | $4,477.36 | Allstate | $5,413.73 | GEICO | $5,046.39 | State Farm | $3,433.73 | USAA | $3,645.13 |

| 71072 | SHONGALOO | $4,595.44 | Progressive | $5,439.25 | Allstate | $5,413.73 | State Farm | $3,403.32 | USAA | $3,645.13 |

| 71075 | SPRINGHILL | $4,474.44 | Allstate | $5,413.73 | GEICO | $5,046.39 | State Farm | $3,419.17 | USAA | $3,645.13 |

| 71403 | ANACOCO | $4,430.85 | Allstate | $5,413.73 | Progressive | $5,142.31 | USAA | $3,418.09 | State Farm | $3,805.20 |

| 71406 | BELMONT | $4,610.84 | Progressive | $5,614.41 | Allstate | $5,413.73 | USAA | $3,555.97 | State Farm | $3,577.97 |

| 71426 | FISHER | $4,568.59 | Allstate | $5,413.73 | Progressive | $5,177.85 | USAA | $3,555.97 | State Farm | $3,864.26 |

| 71429 | FLORIEN | $4,476.94 | Allstate | $5,413.73 | Progressive | $5,177.85 | State Farm | $3,406.01 | USAA | $3,555.97 |

| 71439 | HORNBECK | $4,332.48 | Allstate | $5,413.73 | Progressive | $5,142.31 | USAA | $3,187.12 | State Farm | $3,544.31 |

| 71443 | KURTHWOOD | $4,355.93 | Allstate | $5,413.73 | Progressive | $5,152.75 | USAA | $2,981.19 | State Farm | $3,857.06 |

| 71446 | LEESVILLE | $4,408.37 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $2,981.19 | State Farm | $3,978.60 |

| 71449 | MANY | $4,546.33 | Allstate | $5,413.73 | Progressive | $5,387.48 | State Farm | $3,543.35 | USAA | $3,555.97 |

| 71459 | FORT POLK | $4,397.96 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $2,981.19 | State Farm | $3,926.59 |

| 71460 | NEGREET | $4,610.52 | Allstate | $5,413.73 | Progressive | $5,387.48 | USAA | $3,555.97 | State Farm | $3,864.26 |

| 71461 | NEWLLANO | $4,440.21 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $3,172.35 | State Farm | $3,946.65 |

| 71462 | NOBLE | $4,587.34 | Progressive | $5,600.85 | Allstate | $5,413.73 | State Farm | $3,534.99 | USAA | $3,555.97 |

| 71468 | PROVENCAL | $4,591.96 | Allstate | $5,413.73 | Progressive | $5,170.17 | USAA | $3,580.55 | State Farm | $3,785.75 |

| 71474 | SIMPSON | $4,435.33 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $3,173.59 | State Farm | $3,921.03 |

| 71475 | SLAGLE | $4,471.44 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $3,418.09 | State Farm | $3,857.06 |

| 71486 | ZWOLLE | $4,580.26 | Progressive | $5,600.85 | Allstate | $5,413.73 | State Farm | $3,499.60 | USAA | $3,555.97 |

We also have a list of the most expensive ZIP codes in Louisiana.

| Most Expensive ZIP Codes in Louisiana | City | Average Annual Rate by ZIP Code | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|---|

| 70032 | ARABI | $8,001.83 | Progressive | $11,220.15 | GEICO | $8,646.01 | USAA | $5,601.65 | State Farm | $7,180.78 |

| 70043 | CHALMETTE | $7,852.33 | Progressive | $11,251.46 | GEICO | $8,284.43 | USAA | $5,601.65 | State Farm | $6,763.55 |

| 70053 | GRETNA | $7,895.98 | Progressive | $11,054.29 | GEICO | $9,043.51 | USAA | $5,455.88 | State Farm | $6,108.63 |

| 70058 | HARVEY | $7,919.05 | Progressive | $11,116.86 | GEICO | $9,080.79 | USAA | $5,410.50 | State Farm | $6,169.49 |

| 70072 | MARRERO | $7,857.95 | Progressive | $10,759.92 | GEICO | $8,816.72 | USAA | $5,929.56 | State Farm | $5,965.95 |

| 70112 | NEW ORLEANS | $8,540.11 | Progressive | $11,286.61 | Allstate | $10,194.23 | USAA | $5,708.44 | State Farm | $7,428.67 |

| 70113 | NEW ORLEANS | $9,085.51 | Progressive | $11,349.19 | GEICO | $10,470.09 | USAA | $6,205.63 | State Farm | $7,208.41 |

| 70114 | NEW ORLEANS | $8,180.81 | Progressive | $11,286.61 | GEICO | $9,623.03 | USAA | $5,846.50 | State Farm | $6,330.33 |

| 70116 | NEW ORLEANS | $9,013.80 | Progressive | $11,286.61 | Allstate | $10,194.23 | USAA | $6,225.89 | State Farm | $7,667.52 |

| 70117 | NEW ORLEANS | $9,303.50 | Progressive | $11,349.19 | GEICO | $10,722.66 | USAA | $6,335.87 | State Farm | $7,915.53 |

| 70119 | NEW ORLEANS | $8,860.81 | Progressive | $11,297.04 | Allstate | $10,194.23 | USAA | $6,016.67 | State Farm | $7,081.33 |

| 70122 | NEW ORLEANS | $8,940.09 | Progressive | $11,349.19 | GEICO | $10,626.87 | USAA | $5,798.83 | State Farm | $6,731.32 |

| 70125 | NEW ORLEANS | $8,459.50 | Progressive | $11,116.86 | Allstate | $10,194.23 | USAA | $6,004.41 | State Farm | $6,878.72 |

| 70126 | NEW ORLEANS | $9,155.49 | Progressive | $11,193.79 | GEICO | $10,418.61 | USAA | $6,628.66 | State Farm | $7,342.14 |

| 70127 | NEW ORLEANS | $9,249.24 | Progressive | $11,400.32 | GEICO | $10,518.81 | USAA | $6,555.17 | State Farm | $7,577.65 |

| 70128 | NEW ORLEANS | $9,203.05 | Progressive | $11,483.77 | GEICO | $10,518.81 | USAA | $6,562.78 | State Farm | $7,255.65 |

| 70129 | NEW ORLEANS | $9,123.75 | Progressive | $11,277.24 | GEICO | $10,565.56 | USAA | $6,562.78 | State Farm | $7,018.93 |

| 70130 | NEW ORLEANS | $8,542.14 | Progressive | $11,286.61 | Allstate | $10,194.23 | USAA | $5,708.44 | State Farm | $7,235.76 |

| 70131 | NEW ORLEANS | $7,899.82 | Progressive | $11,411.76 | GEICO | $8,621.16 | USAA | $5,502.31 | State Farm | $6,146.30 |

| 70139 | NEW ORLEANS | $8,675.04 | Progressive | $11,286.61 | Allstate | $10,194.23 | USAA | $5,708.44 | State Farm | $7,198.23 |

| 70145 | NEW ORLEANS | $9,034.55 | Progressive | $11,349.19 | GEICO | $10,722.66 | USAA | $5,708.44 | State Farm | $7,198.23 |

| 70146 | NEW ORLEANS | $9,034.55 | Progressive | $11,349.19 | GEICO | $10,722.66 | USAA | $5,708.44 | State Farm | $7,198.23 |

| 70148 | NEW ORLEANS | $8,877.47 | Progressive | $11,349.19 | GEICO | $10,626.87 | USAA | $5,708.44 | State Farm | $6,508.60 |

| 70163 | NEW ORLEANS | $8,547.15 | Progressive | $11,349.19 | Allstate | $10,194.23 | USAA | $5,708.44 | State Farm | $7,198.23 |

| 70170 | NEW ORLEANS | $8,521.57 | Progressive | $11,286.61 | Allstate | $10,194.23 | USAA | $5,708.44 | State Farm | $7,198.23 |

The area with a ZIP code in the French Quarter is bound to have higher rates than those ZIP codes on the outskirts of New Orleans, even if it is by only a few dollars per month.

For this reason, we include below the average rates by city.

| Cheapest Cities in Louisiana | Average Annual Rate by City | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|

| Anacoco | $4,430.85 | Allstate | $5,413.73 | Progressive | $5,142.31 | USAA | $3,418.09 | State Farm | $3,805.20 |

| Arcadia | $4,604.07 | Allstate | $5,413.73 | Progressive | $5,206.83 | State Farm | $3,594.95 | USAA | $3,758.45 |

| Belmont | $4,610.84 | Progressive | $5,614.41 | Allstate | $5,413.73 | USAA | $3,555.97 | State Farm | $3,577.97 |

| Castor | $4,592.82 | Allstate | $5,413.73 | Progressive | $5,270.63 | State Farm | $3,553.73 | USAA | $3,843.04 |

| Cullen | $4,474.44 | Allstate | $5,413.73 | GEICO | $5,046.39 | State Farm | $3,419.17 | USAA | $3,645.13 |

| Fisher | $4,568.59 | Allstate | $5,413.73 | Progressive | $5,177.85 | USAA | $3,555.97 | State Farm | $3,864.26 |

| Florien | $4,476.94 | Allstate | $5,413.73 | Progressive | $5,177.85 | State Farm | $3,406.01 | USAA | $3,555.97 |

| Fort Polk | $4,397.96 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $2,981.19 | State Farm | $3,926.59 |

| Haynesville | $4,630.28 | Progressive | $5,439.25 | Allstate | $5,413.73 | State Farm | $3,577.56 | USAA | $3,645.13 |

| Hornbeck | $4,332.48 | Allstate | $5,413.73 | Progressive | $5,142.31 | USAA | $3,187.12 | State Farm | $3,544.31 |

| Jamestown | $4,608.94 | Allstate | $5,413.73 | Progressive | $5,270.63 | State Farm | $3,634.33 | USAA | $3,843.04 |

| Kurthwood | $4,355.93 | Allstate | $5,413.73 | Progressive | $5,152.75 | USAA | $2,981.19 | State Farm | $3,857.06 |

| Leesville | $4,408.37 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $2,981.19 | State Farm | $3,978.60 |

| Lisbon | $4,601.27 | Allstate | $5,413.73 | Progressive | $5,298.84 | State Farm | $3,624.07 | USAA | $3,645.13 |

| Many | $4,546.33 | Allstate | $5,413.73 | Progressive | $5,387.48 | State Farm | $3,543.35 | USAA | $3,555.97 |

| Negreet | $4,610.51 | Allstate | $5,413.73 | Progressive | $5,387.48 | USAA | $3,555.97 | State Farm | $3,864.26 |

| New Llano | $4,440.21 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $3,172.35 | State Farm | $3,946.65 |

| Noble | $4,587.34 | Progressive | $5,600.85 | Allstate | $5,413.73 | State Farm | $3,534.99 | USAA | $3,555.97 |

| Provencal | $4,591.96 | Allstate | $5,413.73 | Progressive | $5,170.17 | USAA | $3,580.55 | State Farm | $3,785.75 |

| Ringgold | $4,613.19 | Allstate | $5,413.73 | Progressive | $5,216.23 | State Farm | $3,709.97 | USAA | $3,843.04 |

| Sarepta | $4,477.35 | Allstate | $5,413.73 | GEICO | $5,046.39 | State Farm | $3,433.73 | USAA | $3,645.13 |

| Shongaloo | $4,595.44 | Progressive | $5,439.25 | Allstate | $5,413.73 | State Farm | $3,403.32 | USAA | $3,645.13 |

| Simpson | $4,435.33 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $3,173.59 | State Farm | $3,921.03 |

| Slagle | $4,471.44 | Allstate | $5,579.18 | Progressive | $5,152.75 | USAA | $3,418.09 | State Farm | $3,857.06 |

| Zwolle | $4,580.26 | Progressive | $5,600.85 | Allstate | $5,413.73 | State Farm | $3,499.60 | USAA | $3,555.97 |

Hornbeck has the cheapest rates in Louisiana, costing over $4,000 less than rates in New Orleans.

| Most Expensive Cities in Louisiana | Average Annual Rate by City | Most Expensive Company | Most Expensive Annual Rate | 2nd Most Expensive Company | 2nd Most Expensive Annual Rate | Cheapest Company | Cheapest Annual Rate | 2nd Cheapest Company | 2nd Cheapest Annual Rate |

|---|---|---|---|---|---|---|---|---|---|

| Arabi | $8,001.83 | Progressive | $11,220.15 | GEICO | $8,646.01 | USAA | $5,601.65 | State Farm | $7,180.78 |

| Avondale | $7,150.36 | Progressive | $10,423.27 | GEICO | $8,215.55 | Allstate | $5,175.46 | USAA | $5,929.56 |

| Baker | $6,694.24 | Progressive | $9,061.48 | GEICO | $7,592.92 | USAA | $4,737.73 | State Farm | $5,276.11 |

| Barataria | $7,257.44 | Progressive | $11,379.45 | Allstate | $7,817.59 | State Farm | $4,725.25 | USAA | $5,264.66 |

| Baton Rouge | $6,786.59 | Progressive | $9,301.30 | GEICO | $7,607.46 | USAA | $4,869.88 | State Farm | $5,317.05 |

| Belle Chasse | $7,147.88 | Progressive | $9,986.77 | Allstate | $8,110.10 | USAA | $4,869.75 | State Farm | $5,430.25 |

| Boothville | $6,756.68 | Progressive | $8,916.82 | Allstate | $8,110.10 | State Farm | $4,786.49 | USAA | $4,869.75 |

| Braithwaite | $7,070.65 | Progressive | $11,312.43 | Allstate | $7,360.57 | State Farm | $4,710.25 | USAA | $4,869.75 |

| Burnside | $7,011.06 | Progressive | $11,546.32 | GEICO | $6,829.86 | USAA | $4,819.16 | State Farm | $5,056.99 |

| Chalmette | $7,852.33 | Progressive | $11,251.46 | GEICO | $8,284.43 | USAA | $5,601.65 | State Farm | $6,763.55 |

| Elmwood | $6,943.52 | Progressive | $10,878.87 | GEICO | $7,590.53 | USAA | $5,006.83 | State Farm | $5,116.54 |

| Estelle | $7,857.95 | Progressive | $10,759.92 | GEICO | $8,816.72 | USAA | $5,929.56 | State Farm | $5,965.95 |

| Gretna | $7,860.34 | Progressive | $10,956.51 | GEICO | $8,939.46 | USAA | $5,455.88 | State Farm | $6,132.24 |

| Harvey | $7,919.05 | Progressive | $11,116.86 | GEICO | $9,080.79 | USAA | $5,410.50 | State Farm | $6,169.49 |

| Kenner | $7,250.98 | Progressive | $10,866.48 | GEICO | $7,913.35 | USAA | $5,527.33 | State Farm | $5,756.15 |

| Lafitte | $7,282.71 | Progressive | $11,379.45 | Allstate | $7,817.59 | State Farm | $4,851.62 | USAA | $5,264.66 |

| Meraux | $7,789.28 | Progressive | $11,282.73 | GEICO | $8,452.79 | USAA | $5,601.65 | State Farm | $6,248.68 |

| Metairie | $7,028.30 | Progressive | $10,954.16 | GEICO | $7,457.85 | USAA | $5,202.82 | State Farm | $5,401.80 |

| New Orleans | $8,649.31 | Progressive | $11,225.41 | Allstate | $9,603.97 | USAA | $5,944.69 | State Farm | $6,997.47 |

| Pilottown | $6,775.22 | Progressive | $8,916.82 | Allstate | $8,110.10 | USAA | $4,869.75 | State Farm | $4,879.19 |

| Pointe A La Hache | $7,254.34 | Progressive | $11,312.43 | Allstate | $8,110.10 | USAA | $4,869.75 | State Farm | $4,879.19 |

| Port Sulphur | $6,988.27 | Progressive | $9,986.77 | Allstate | $8,110.10 | USAA | $4,869.75 | State Farm | $4,874.50 |

| Poydras | $7,346.93 | Progressive | $11,312.43 | Allstate | $7,360.57 | USAA | $4,869.75 | State Farm | $6,208.18 |

| Uncle Sam | $7,025.29 | Progressive | $11,546.32 | GEICO | $6,829.86 | USAA | $4,890.31 | State Farm | $5,056.99 |

| Venice | $6,749.62 | Progressive | $8,916.82 | Allstate | $8,110.10 | State Farm | $4,751.19 | USAA | $4,869.75 |

With so many options in auto insurance providers, it can be difficult to choose a company that you can confide in to cover you when the unexpected happens.

Our data analysts pulled the top 5-10 insurance companies for Louisiana residents to help you begin to make some comparisons and choose the right coverage for you and your family.

Are you ready?

| Property & Casualty Insurance | Number |

|---|---|

| Domestic | 34 |

| Foreign | 819 |

| Total | 953 |

The chart below shows the ten largest auto insurance companies in Louisiana and is sorted by market share.

Also included is direct premiums written and loss ratio for 2017.

| Company | Direct Premiums Written | Loss Ratio | Market Share |

|---|---|---|---|

| Allstate Insurance Group | $502,616 | 53.33% | 11.15% |

| Amtrust NGH Group | $104,343 | 67.11% | 2.32% |

| Geico | $432,095 | 75.64% | 9.59% |

| Goauto Insurance Co | $144,626 | 74.36% | 3.21% |

| Liberty Mutual Group | $253,836 | 68.10% | 5.63% |

| Progressive Group | $602,564 | 65.32% | 13.37% |

| Safeway Insurance Group | $72,940 | 67.02% | 1.62% |

| Southern Farm Bureau Casualty Group | $231,086 | 70.01% | 5.13% |

| State Farm Group | $1,512,622 | 73.76% | 33.57% |

| USAA Group | $248,894 | 86.36% | 5.52% |

Keep in mind that these loss ratios are for all coverage types combined. It is clear that the loss ratios of these top ten companies contribute to the state’s overall loss ratio of 99.68 for claims made against uninsured/underinsured motorists coverage.

Reviewing ratings provided by third-party entities such as A.M. Best is a great place to start narrowing down your options. These agencies take into consideration many factors that lead to their judgment of a company’s credibility and financial outlook.

| Company | Financial Rating |

|---|---|

| Allstate Insurance Group | A+ |

| Amtrust NGH Group | Not Rated (NR) |

| Geico | A++ |

| Goauto Insurance Co | Not Rated (NR) |

| Liberty Mutual Group | A |

| Progressive Group | A+ |

| Safeway Insurance Group | A |

| Southern Farm Bureau Casualty Group | A+ |

| State Farm Group | A++ |

| USAA Group | A++ |

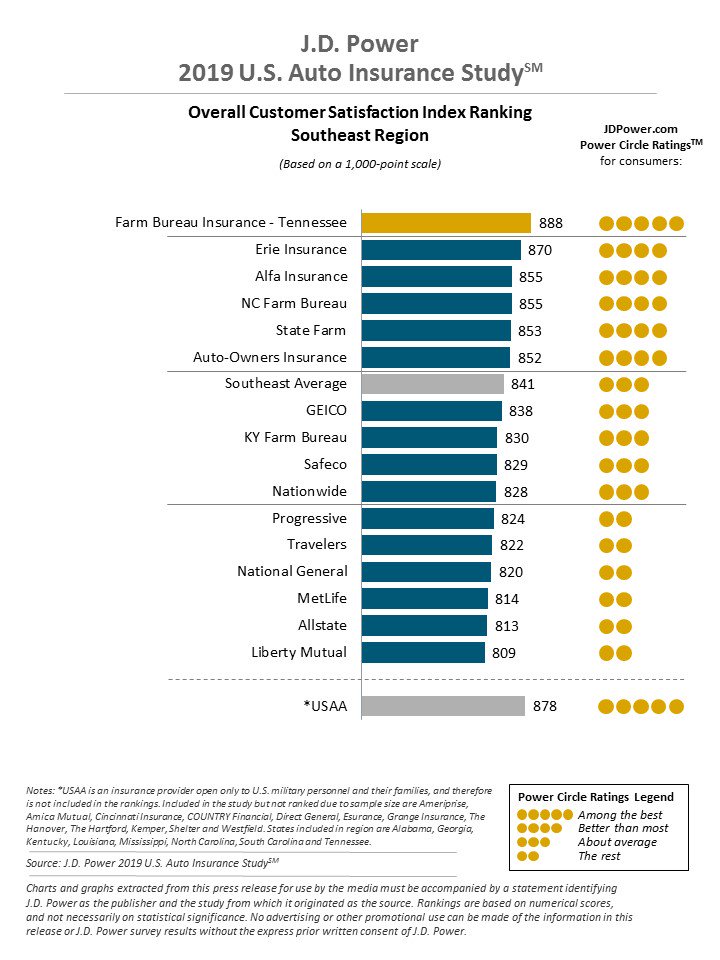

Just as important as a company’s future financial stability are ratings in customer satisfaction.

JD Power Power Circle Ratings look at a wide variety of customer satisfaction variables pulled from surveys completed by actual consumers of a company’s products and services. The ratings below cover the southeast region which is comprised of eight states to include Louisiana.

Now that you have reviewed the more positive side with financial outlook and customer ratings for several companies, it is critical to weigh the bad as well.

The table below shows the number of complaints and the complaint ratio compared to their market share and direct premiums written for each of the top ten companies that provide auto insurance in Louisiana for 2017.

A company with a complaint index of 1 has an average number of complaints. A company with a complaint index higher than 1 has more complaints than average. The table is sorted based on the lowest complaint ratio. Feel free to sort the table.

| Company | Direct Premiums Written | Market Share | Number of Complaints | Complaint Index |

|---|---|---|---|---|

| Allstate Insurance Co | $126,806,438 | 2.81% | 41 | 1.488225 |

| Allstate Property & Casulty | $334,999,133 | 7.43% | 25 | 0.343496 |

| Geico | $310,652,097 | 6.89% | 70 | 1.037169 |

| GoAuto | $144,626,094 | 3.21% | 74 | 2.355109 |

| Liberty | $114,475,768 | 2.54% | 38 | 1.527904 |

| Louisiana Farm Bureau | $224,526,282 | 4.98% | 25 | 0.512505 |

| Progressive | $435,995,441 | 9.68% | 59 | 0.622868 |

| Progressive | $166,568,349 | 3.70% | 39 | 1.0777 |

| Safeco | $109,688,794 | 2.43% | 10 | 0.419627 |

| State Farm | $1,417,799,324 | 31.46% | 223 | 0.723962 |

Bear in mind that this data is determined by official complaints submitted in writing to the Louisiana Department of Insurance and may not provide a full picture of consumer opinions.

Now to the good stuff! We revealed earlier that Louisiana has the highest rates in the country.

In this section, we cover average annual rates for the top five companies in Louisiana based on unique factors to you: your commute, driving record, and chosen coverage level.

But first, let’s look at the average rates by the company overall.

| Company | Annual Average | Higher/Lower Rate than State Average | Higher/Lower Percentage than State Average |

|---|---|---|---|

| Allstate P&C | $5,998.79 | $287.44 | +4.79% |

| Geico Cas | $6,154.60 | $443.25 | +7.20% |

| Progressive Security Ins. | $7,471.10 | $1,759.75 | +23.55% |

| State Farm Mutual Auto | $4,579.12 | -$1,132.22 | -24.73% |

| USAA | $4,353.12 | -$1,358.23 | -31.20% |

As you can see in the table above, USAA and State Farm have the best rates compared to the state average. Note that USAA offers services to only active and retired military and their family members. If this doesn’t apply to you, State Farm may be a good option.

| Company | 10 Miles Commute, 6,000 Annual Mileage | 25 Miles Commute, 12,000 Annual Mileage |

|---|---|---|

| Allstate | $5,998.79 | $5,998.79 |

| Geico | $6,034.79 | $6,274.40 |

| Progressive | $7,471.10 | $7,471.10 |

| State Farm | $4,461.13 | $4,697.11 |

| USAA | $4,218.32 | $4,487.91 |

If you have a long commute, getting a policy with Allstate or Progressive is a good option because both of these companies don’t charge more for a longer commute.

Commute times and distance do not affect your rates nearly as much as some other factors. Take a look.

In most states, the adage “buy in bulk” applies in that the higher the liability limits you select, the better deal you are getting on coverage.

Unfortunately, that is not the case in Louisiana, as you can see in the table below.

| Group | Annual Rate with Low Coverage | Annual Rate with Medium Coverage | Annual Rate with High Coverage |

|---|---|---|---|

| Allstate | $5,185.16 | $6,109.21 | $6,702.00 |

| Geico | $5,086.66 | $6,176.92 | $7,200.21 |

| Progressive | $6,193.86 | $7,406.27 | $8,813.16 |

| State Farm | $3,962.47 | $4,568.03 | $5,206.86 |

| USAA | $3,776.25 | $4,420.47 | $4,862.64 |

In most states, it could cost as little as $3-$17 per month to move from low or medium coverage to high coverage.

Louisiana auto insurance rates are 13-30 percent higher for medium to high coverage levels.

Your credit history can sometimes make a big difference in your auto insurance premium. If you see an increase in your premium, and you did not get a ticket and you were not in an accident, your credit score may have reduced into a lower threshold.

Insurance companies use this information to judge your likelihood of making a claim; however, getting to poor credit status takes some time unless you have risky spending habits in a short period of time.

| Company | Annual Rate with Good Credit | Annual Rate with Fair Credit | Annual Rate with Poor Credit |

|---|---|---|---|

| Allstate | $4,726.27 | $7,236.85 | $8,444.80 |

| Geico | $4,788.40 | $6,353.32 | $7,859.57 |

| Progressive | $6,731.64 | $5,410.52 | $7,322.08 |

| State Farm | $3,300.33 | $4,086.69 | $6,350.34 |

| USAA | $3,207.81 | $3,841.14 | $6,010.39 |

It appears that Progressive is the most forgiving in its rates if you have poor credit.

No one plans to get caught speeding, cause an accident, or get caught drinking and driving; but, if one of these unfortunate things happen, expect your premium to increase.

| Company | Clean record | One Speeding Ticket | One Accident | One DUI |

|---|---|---|---|---|

| Allstate | $4,753.81 | $7,221.89 | $7,221.89 | $6,443.95 |

| Geico | $4,180.19 | $6,755.09 | $6,755.09 | $8,315.63 |

| Progressive | $6,223.20 | $8,352.66 | $8,352.66 | $8,027.23 |

| State Farm | $4,196.97 | $4,961.27 | $4,961.27 | $4,579.12 |

| USAA | $3,321.63 | $4,611.20 | $4,611.20 | $5,514.32 |

In Louisiana, it looks like State Farm is the most lenient when it comes to infractions.

Also worth noting, most insurance companies (with the exception of Geico) have more leniency on drivers who are cited for a DUI.

Enter your ZIP code below to view companies that have cheap auto insurance rates.

Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Though Louisiana’s rates are not that affordable in general, it is important to understand how and why the laws affect rates.

You can still get a reasonable rate if you do your research.

Keep reading to learn about the driving and insurance laws specific to the state of Louisiana.

So, the moment you’ve been waiting for…

Really, why are the rates so high?

Here’s one major reason…

Louisiana is a “direct action” state. This statute permits an injured plaintiff, after seeking the little to no liability coverage of the at-fault driver, to sue an insurance company for the lack of coverage under the policy purchased by the at-fault driver.

This means that if a lawsuit is filed against a defendant, and the bills still aren’t paid, another lawsuit can be filed against the insurance company, which has a lot more funds to shell out for damages and injuries.

So this means that auto insurance companies have to charge even higher rates to protect their profit to loss margin.

You may be wondering, why haven’t lawmakers in Louisiana done anything about this?

Well, the state of Louisiana is a classic chicken and egg situation… and it dates back to 1918.

In fact, Louisiana was the state that set the standard for direct action statutes that are practiced (in some form) in only eight other states in the US.

This statute “expresses the long-held policy of the Bayou State that ‘insurance policy against liability is not issued primarily for the protection of the insured but for the protection of the public.’ Davies v. Consolidated Underwriters, 6 So.2d 351 (La. 1942).”

Read more about this law here.

Lawmakers in Louisiana and the auto insurance companies are making concerted efforts to respond to this chicken-egg dilemma.

Insurance companies in Louisiana have come up with an option to attempt to balance the scales, so to speak, and that is the option to have “economic-only” coverage uninsured/underinsured motorists coverage as we mentioned earlier.

Economic-only uninsured motorist insurance coverage is a relatively new development in Louisiana and was part of the 1997 legislative reform effort in Acts 1997, No. 1476, known as the “Omnibus Premium Reduction Act of 1997,” affectionately nicknamed the “No Pay, No Play” Act.

The offering of economic-only uninsured and underinsured motorist coverage was, on average, 20 percent below the uninsured and underinsured motorist coverage rates in place in 1997.

We ran a hypothetical quote with one of the insurance providers, and the economic-only quote ran only seven percent lower than the full uninsured motorist coverage at the same minimum level.

If you do consider purchasing economic-only uninsured motorist coverage, be sure to inquire about the difference in the two quoted amounts with each company.

With many customers looking to get the cheapest rate, your insurance company may try to entice you with the Louisiana-specific option of purchasing “economic-only” uninsured motorist coverage.

Word of caution…

If you do agree to “economic-only” coverage, this means that if an uninsured motorist hits you, you can make a claim ONLY for “economic-only” damages — those that equate to hard dollars such as property damage, lost wages, and medical bills.

Unfortunately, with this option, you will not be permitted to file a claim to cover arbitrarily-estimated costs such as pain, suffering, inconvenience, and mental anguish.

So this is one of the “bandaids” that Louisiana lawmakers and insurance companies have put in place to even out the playing field.

Basically, it equates to, “we will give you a lower premium if you sign over your right to claim for non-economic damages and injuries.”

But with rates as high as they are (still), some Louisiana residents may be inclined to lay down and take the money, or not get coverage at all, which is even worse.

Keep reading to find out the price you will pay for not purchasing auto insurance in Louisiana.

You may be thinking: If I have to pay astronomical rates just to get unquestioned coverage in case an uninsured motorist hits me, what do they have to lose?

Well, don’t worry too much about the irresponsibility of the uncovered at-fault driver; their negligence is not tolerated.

As another part of the “No Pay, No Play” Act, if an uninsured person sustains property damage or bodily injury, and you are at fault (whether you have enough coverage or not), the uninsured individual starts in the hole…

Driving without auto insurance in Louisiana carries a negative balance of $25,000 in property damages and $15,000 in personal injuries.

So, if you choose not to get auto insurance in Louisiana, that’s, merely to start, $40,000 worth of risk you take by not having any liability coverage.

Hold yourself accountable and purchase that auto insurance policy. If you don’t, you will lose what you already don’t have.

Auto insurance laws vary from state to state, and Louisiana is no different, as we have seen already. In this section, we cover more laws associated with auto insurance.

If you have a history of accidents or traffic violations, and you are finding it difficult to purchase coverage from an auto insurance carrier, the Louisiana Automobile Insurance Plan be a good option.

This plan is provided through a third-party company called AIPSO. If you go to their website, you will notice a disclaimer at the top of the page releasing them from any liability. This company works with other states as well, but their sites do not have a disclaimer.

This is just further evidence why Louisiana auto insurance rates are so high due to the potential of a company being sued.

Louisiana does not have any special low-cost programs for people who don’t have insurance. It is up to you, as the consumer, to shop around for the lowest rate. You can’t afford to NOT have insurance, especially starting $40K in the hole!

Louisiana law does not require insurance companies to provide windshield repair or replacement, but it is an option, especially if the damage is caused by a road hazard. The law does permit insurance companies to use aftermarket crash parts if included in the estimate. The deductible may vary but can not exceed $250.

Insurance fraud is considered a crime in Louisiana, and the state has a fraud bureau set up to investigate cases.

In 2017, over $3.5 billion was spent on investigating auto insurance fraud cases which made up 68 percent of all insurance fraud cases in Louisiana. Of the total auto claims fraud cases in 2017, 57 percent were from referrals made by individuals just like you.

With rates so high due to numerous lawsuits, do your part and report any suspected fraud.

You may be asking, could I get sued for reporting fraud?

Not to worry — two state laws provide complete immunity from a lawsuit if you, in good faith, report a person who is committing insurance fraud.

The Louisiana Department of Insurance has also made great efforts towards increasing awareness about insurance fraud. They provide a brochure and a 20-page handbook with tips on how to protect yourself and your family regarding all types of insurance, not just auto.

A statute of limitations is the limit on the amount of time you have, from the time of an accident, to bring a lawsuit to court. Most states differentiate time limits for personal injury and property damage matters.

However, Louisiana lumps it all into one, and you have only one year to file for the lawsuit, which is significantly less time than other states permit (2-3 years).

Louisiana is a “pure comparative fault” state based on the Louisiana Civil Code section 2323.

If you decide to file suit against an at-fault driver, pure comparative fault means that the amount of damages you are able to recover is reduced by the percentage the judge or jury finds you at fault.

For instance, if you turned right on red when it is prohibited and the other driver ran a red light, a judge or jury will decide the percentage of fault each driver had in the accident.

This percentage is then assigned and equated to the amount of money each driver can retain, so hire a good attorney!

Let’s find out what licensing requirements exist in Louisiana for various populations.

| Young Driver Licensing Laws | Age Restrictions | Passenger Restrictions | Time Restrictions |

|---|---|---|---|

| Learner's Permit | 15; obtain a temporary instruction permit (TIP) from the OMV; completion of driver education course; TIP is exchanged for a learner's permit | No more than one passenger younger than 21 between the hours of 6 pm-5 am; no passenger restriction from 5 am-6 pm | 11 p.m. - 5 a.m. |

| Provisional License | 6 months holding period 50 hours, 15 of which must be at night | No more than one passenger younger than 21 between the hours of 6 pm-5 am; no passenger restriction from 5 am-6 pm | 11 p.m. - 5 a.m. |

| Full License | 16 | Lifted at age 17 | Lifted at age 17 |

| Renewal Procedures | General Population | Older Population |

|---|---|---|

| License renewal cycle | 6 years | 6 years |

| Mail or online renewal permitted | Both, every other renewal | Not permitted 70 and older |

| Proof of adequate vision required at renewal | When renewing in person | 70 and older, every renewal |

Louisiana does make an exception for those who 70 and older with a medically diagnosed disability that makes it difficult for them to renew in person. However, a sworn physician-certified affidavit must be submitted stating that the person possesses all cognitive functions reasonably necessary to be a prudent driver.

If you are planning to relocate to Louisiana, here are the things you need to do:

Knowing some of Louisiana’s basic driving laws can keep you safe and will help you keep your rates from increasing.

Ready?

The first thing to know is that Louisiana follows a traditional fault-based system when it comes to financial responsibility for losses stemming from a crash: that includes car accident injuries, lost income, vehicle damage, and so on.

To note, however, is that if a non-fault driver is not able to obtain the monetary value of their losses after an accident with the at-fault driver, the plaintiff is permitted to file suit against the auto insurance company.

Those driving in Louisiana must keep right at all times unless passing on the left or turning left. Drivers must also move right if they are blocking vehicles behind them.

Move over laws usually always apply to emergency vehicles; however, in Louisiana, this applies to any vehicle with flashing lights including tow trucks. If a driver is not able to completely vacate the lane closest to the stopped vehicle, they must slow to a safe speed.

Maximum posted speed limits are 75 mph on rural interstates, 70 mph on urban interstates, 70 mph on limited-access roads, and 65 mph on all other roads.

A child safety seat must be in use for all children five years and younger or less than 60 pounds must be restrained in a

In failing to obey this law, you could be fined $100, or worse, put your child in danger.

Once a child turns 6 years old and weighs at least 60 pounds, he or she can ride in any seats. Child safety seat laws in Louisiana do not specify a preference for the back seat.

No person shall ride in the cargo areas of a pickup truck unless:

Rideshare services like Uber require that all their drivers maintain their own auto insurance policies that meet at least the minimum coverages required by Louisiana law. However, if a driver wishes to obtain special coverage for this role, both USAA and State Farm offer specialized rideshare coverage.

According to the Insurance Institute for Highway Safety (IIHS), “automation is the use of a machine or technology to perform a task or function that was previously carried out by a human. In driving, automation involves using radar, camera and other sensors to gather information about a vehicle’s surroundings, which is then used by computer programs to perform parts or all of the driving task on a sustained basis.”

Currently, Louisiana has no restrictions on autonomous vehicles.

Buckling up and obeying the speed limits are two basic practices that ensure your safety and the safety of others on the streets of Louisiana. Other laws exist to prevent reckless or impaired driving.

| Penalty | First Offense | Second Offense | Third Offense | Fourth and Subsequent Offenses |

|---|---|---|---|---|

| License Suspension | 1 year/hBAC 2 years | 2 years/hBAC 4 years | 3 years | Vehicle seized |

| Imprisonment | 48 hours in jail + up to 6 months OR fine; up to 2 years probation | 48 hours+ | 1-5 years w/ or w/o hard labor | 10-30 years, two years served w/o suspension or parole + home incarceration for at least 1 year |

| Fine | $300-$1000 +$100 reinstatement fee | $750-$1000 +$200 reinstatement fee | $2000 +$300 reinstatement fee | $5000 +$300 reinstatement fee |

| Other | 30 hours reeducation, 32+ hours community service, half must be street garbage pickup | Possible 30 days community service +reeducation requirements of 1st DWI | 30 days community service, evaluation for addictive disorder, IID, probabtion and home incarceration for any part of suspended sentence | 40 days community service |

As you can see in the table above, Louisiana has lenient laws regarding drinking and driving, especially compared to other states. An offense is not classified as a crime until the third and fourth citation.

Louisiana currently has no marijuana-specific impaired driving laws.

All distracted driving laws in Louisiana are primarily enforced meaning that you can be pulled over for the following violations.

Louisiana has a handheld ban for all drivers in signed school zones.

All learner’s permit holders and all intermediate license holders, no matter the age, are not to use a hand-held cellphone while driving. Drivers younger than 18 are prohibited from using any cellphone, which includes speakerphone or using a phone through car speakers.

Cellphone use is also not permitted for all drivers during the first year of being a licensed driver, no matter the age.

The cellphone ban is secondarily enforced for novice drivers ages 18 and older. Secondary enforcement means that you must be pulled over for another offense before you can be given a citation.

How safe is it to drive in Louisiana?

Well, the data our researchers found might surprise you.

Let’s examine the statistics of theft and fatalities from risky driving behavior.

Here are the top-10 stolen cars in Louisiana:

| Vehicle | Number of Thefts (2016) |

|---|---|

| Chevrolet Pickup (Full Size) | 671 |

| Ford Pickup (Full Size) | 584 |

| GMC Pickup (Full Size) | 253 |

| Toyota Camry | 224 |

| Dodge Pickup (Full Size) | 222 |

| Nissan Altima | 215 |

| Honda Accord | 209 |

| Chevrolet Impala | 177 |

| GMC Yukon | 125 |

| Chevrolet Tahoe | 114 |

Listed below are the three cities in which the most vehicles were stolen in 2013.

| City | # of Stolen Cars |

|---|---|

| New Orleans | 2,143 |

| Shreveport | 504 |

| Baton Rouge | 506 |

The best way to stay safe while driving is to always keep your eyes on the road and stay aware of common risky driving issues in your state.

In 2017, there were 44 traffic-incident-related fatalities in Orleans Parish alone, comprising an 11.19 fatality rate per 100,000 of the population.

Let’s inspect the data a little more closely.

Being located in the South, Louisiana drivers don’t need to worry about snow but rain and other natural conditions can have a huge impact on travel in the state.

| Weather Condition | Daylight | Dark, but Lighted | Dark | Dawn or Dusk | Other / Unknown | Total |

|---|---|---|---|---|---|---|

| Normal | 276 | 93 | 219 | 32 | 1 | 621 |

| Rain | 20 | 15 | 16 | 4 | 0 | 55 |

| Snow/Sleet | 1 | 0 | 0 | 0 | 0 | 1 |

| Other | 2 | 4 | 8 | 0 | 0 | 14 |

| Unknown | 0 | 1 | 1 | 0 | 3 | 5 |

| TOTAL | 299 | 113 | 244 | 36 | 4 | 696 |

Whether you are driving, biking, or walking, always be cautious when traveling. You don’t want to become a statistic for the table below.

| Type | Number of Fatalities |

|---|---|

| Traffic Fatalities | 760 |

| Passenger Vehicle Occupant Fatalities (All Seat Positions) | 488 |

| Motorcyclist Fatalities | 96 |

| Drivers Involved in Fatal Crashes | 1,041 |

| Pedestrian Fatalities | 11 |

| Bicyclist and other Cyclist Fatalities | 22 |

Let’s take a look at how traffic fatalities break down by person type:

| Person Type | Number |

|---|---|

| Occupants (Enclosed Vehicles) | 529 |

| Motorcyclists | 96 |

| Nonoccupants | 135 |

In rural areas, the number of traffic fatalities was lower than in urban areas (though not by much): 369 in rural versus 390 in urban.

Single-vehicle crashes are the most reported in Louisiana, followed by incidents involving a roadway departure.

| Crash Type | Number |

|---|---|

| Single Vehicle | 440 |

| Involving a Large Truck | 102 |

| Involving Speeding | 177 |

| Involving a Rollover | 204 |

| Involving a Roadway Departure | 421 |

| Involving an Intersection (or Intersection Related) | 141 |

Below are the 10 Louisiana counties that saw the most traffic fatalities between 2013 and 2017

| County | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| Ascension Parish | 23 | 23 | 19 | 21 | 28 |

| Caddo Parish | 29 | 40 | 36 | 27 | 36 |

| Calcasieu Parish | 24 | 24 | 36 | 47 | 38 |

| East Baton Rouge Parish | 41 | 50 | 43 | 52 | 65 |

| Jefferson Parish | 22 | 24 | 26 | 34 | 28 |

| Orleans Parish | 53 | 50 | 50 | 55 | 44 |

| Ouachita Parish | 22 | 23 | 21 | 20 | 28 |

| St. Tammany Parish | 20 | 22 | 26 | 23 | 30 |

| Tangipahoa Parish | 26 | 22 | 36 | 40 | 31 |

| Terrebonne Parish | 22 | 19 | 16 | 20 | 29 |

Let’s look at speeding-related fatalities over that same five year period.

| County | Fatalities |

|---|---|

| Acadia Parish | 2 |

| Allen Parish | 0 |

| Ascension Parish | 7 |

| Assumption Parish | 1 |

| Avoyelles Parish | 0 |

| Beauregard Parish | 0 |

| Bienville Parish | 0 |

| Bossier Parish | 4 |

| Caddo Parish | 9 |

| Calcasieu Parish | 6 |

| Caldwell Parish | 2 |

| Cameron Parish | 0 |

| Catahoula Parish | 0 |

| Claiborne Parish | 0 |

| Concordia Parish | 0 |

| De Soto Parish | 2 |

| East Baton Rouge Parish | 5 |

| East Carroll Parish | 0 |

| East Feliciana Parish | 4 |

| Evangeline Parish | 2 |

| Franklin Parish | 1 |

| Grant Parish | 1 |

| Iberia Parish | 2 |

| Iberville Parish | 1 |

| Jackson Parish | 0 |

| Jefferson Davis Parish | 1 |

| Jefferson Parish | 3 |

| La Salle Parish | 0 |

| Lafayette Parish | 5 |

| Lafourche Parish | 11 |

| Lincoln Parish | 2 |

| Livingston Parish | 8 |

| Madison Parish | 1 |

| Morehouse Parish | 0 |

| Natchitoches Parish | 0 |

| Orleans Parish | 7 |

| Ouachita Parish | 6 |

| Plaquemines Parish | 1 |

| Pointe Coupe Parish | 2 |

| Rapides Parish | 4 |

| Red River Parish | 2 |

| Richland Parish | 1 |

| Sabine Parish | 1 |

| St. Bernard Parish | 1 |

| St. Charles Parish | 4 |

| St. Helena Parish | 1 |

| St. James Parish | 0 |

| St. John the Baptist Parish | 1 |

| St. Landry Parish | 2 |

| St. Martin Parish | 7 |

| St. Mary Parish | 1 |

| St. Tammany Parish | 10 |

| Tangipahoa Parish | 14 |

| Tensas Parish | 0 |

| Terrebonne Parish | 11 |

| Union Parish | 0 |

| Vermilion Parish | 0 |

| Vernon Parish | 6 |

| Washington Parish | 4 |

| Webster Parish | 1 |

| West Baton Rouge Parish | 4 |

| West Carroll Parish | 1 |

| West Feliciana Parish | 0 |

| Winn Parish | 2 |

Keeping with the same time period, here are the traffic fatalities caused by drinking and driving.

| County | Fatalities |

|---|---|

| Acadia Parish | 4 |

| Allen Parish | 0 |

| Ascension Parish | 7 |

| Assumption Parish | 0 |

| Avoyelles Parish | 3 |

| Beauregard Parish | 1 |

| Bienville Parish | 0 |

| Bossier Parish | 3 |

| Caddo Parish | 14 |

| Calcasieu Parish | 12 |

| Caldwell Parish | 1 |

| Cameron Parish | 1 |

| Catahoula Parish | 0 |

| Claiborne Parish | 0 |

| Concordia Parish | 0 |

| De Soto Parish | 1 |

| East Baton Rouge Parish | 19 |

| East Carroll Parish | 0 |

| East Feliciana Parish | 2 |

| Evangeline Parish | 3 |

| Franklin Parish | 2 |

| Grant Parish | 2 |

| Iberia Parish | 2 |

| Iberville Parish | 2 |

| Jackson Parish | 1 |

| Jefferson Davis Parish | 2 |

| Jefferson Parish | 6 |

| La Salle Parish | 1 |

| Lafayette Parish | 5 |

| Lafourche Parish | 5 |

| Lincoln Parish | 2 |

| Livingston Parish | 4 |

| Madison Parish | 1 |

| Morehouse Parish | 1 |

| Natchitoches Parish | 0 |

| Orleans Parish | 16 |

| Ouachita Parish | 8 |

| Plaquemines Parish | 1 |

| Pointe Parish | 3 |

| Rapides Parish | 2 |

| Red River Parish | 2 |

| Richland Parish | 1 |

| Sabine Parish | 2 |

| St. Bernard Parish | 0 |

| St. Charles Parish | 2 |

| St. Helena Parish | 6 |

| St. James Parish | 1 |

| St. John the Baptist Parish | 0 |

| St. Landry Parish | 7 |

| St. Martin Parish | 6 |

| St. Mary Parish | 3 |

| St. Tammany Parish | 6 |

| Tangipahoa Parish | 7 |

| Tensas Parish | 0 |

| Terrebonne Parish | 13 |

| Union Parish | 0 |

| Vermilion Parish | 2 |

| Vernon Parish | 3 |

| Washington Parish | 2 |

| Webster Parish | 3 |

| West Baton Rouge Parish | 5 |

| West Carroll Parish | 0 |

| West Feliciana Parish | 1 |

| Winn Parish | 0 |

As shown in the table below, compared to other states, Louisiana is ranked 45th in the nation for most teens per million who have been arrested for a DUI.

However, the fatality rate of teens who drink and drive is slightly higher than the national average.

| Teens and Drunk Driving | Data |

|---|---|

| Alcohol-Impaired Driving Fatalities Per 100K Population | 1.3 |

| Higher/Lower Than National Average (1.2) | higher |

| DUI Arrest (Under 18 years old) | 32 |

| DUI Arrests (Under 18 years old) Total Per Million People | 28.73 |

If you are involved in a traffic accident in Louisiana, here’s how long it will take for EMS to get to you.

| Location | Time of Crash to Notification | Arrival | Arrival at Scene to Hospital | Time of Crash to Hospital |

|---|---|---|---|---|

| Rural | 5 minutes | 14 minutes | 45 minutes | 1 hour, 3 minutes |

| Urban | 4 minutes | 8 minutes | 33 minutes | 35 minutes |

If you live in Louisiana, chances are you live in a two-car, or more, household, drive alone to work and spend 10-34 minutes commuting.

Like most of the United States, two-car households make up the largest share of car owners in the state. Unlike the rest of the country, the second largest group is single-car owners, followed by those who own three cars. Often these two statistics are reversed in other states.

With an average commute time of 25.4 minutes, Louisiana ranks below the national average of 25.7 minutes, but not by much. 3.21 percent of Louisiana commuters have a super commute that is 90 minutes or more.

82.7 percent of people in Louisiana drive to work alone and nine percent carpool. One segment of the population that is less concerned about commute time is the 3.36 percent that works from home.

Is traffic a major problem in Louisiana?

According to the INRIX Scorecard, New Orleans ranked 26th in the US for worst traffic. Those who drive in New Orleans sit in traffic for 73 hours per year! This time spent in congestion equates to $1,023 per driver.

Don’t waste another minute while you wait. Start comparison shopping auto insurance rates today!

Cheap Auto Insurance / States